Before Ola Electric’s IPO in August this year, founder and CEO Bhavish Aggarwal compared the company’s growing market share to Indian cricketer Virat Kohli’s batting stats which only seem to go up year after year.

At the time, Aggarwal’s confidence was fairly reasonable, despite the growing competition in the EV two-wheeler industry.

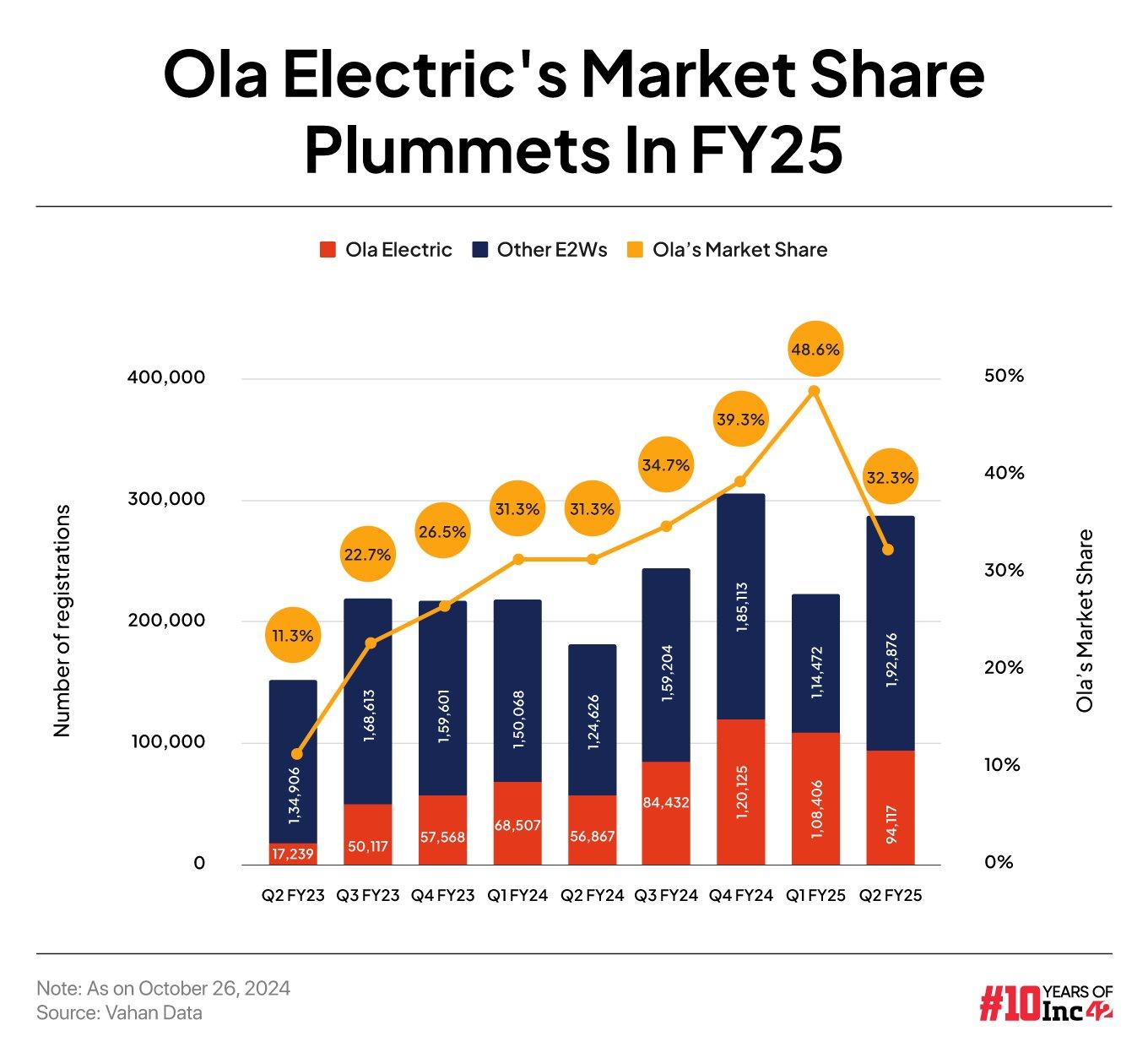

Through persistent issues and complaints regarding quality of vehicles and the after-sales service, Ola Electric![]() continued to gain market share all through FY24. It ended the fiscal year on top of the pile of EV companies in the scooter category.

continued to gain market share all through FY24. It ended the fiscal year on top of the pile of EV companies in the scooter category.

Since the IPO though, things have been far from rosy. Incidentally, even Kohli is under pressure after a dip in form.

The concerns related to after-sales services and vehicle quality have snowballed. Besides dealing with thousands of disgruntled customers, Ola Electric has seen a drop in new vehicle registrations. Rivals such as Ather Energy and legacy players have gained market share at the expense of Aggarwal’s company.

Plus, there’s the matter of how Ola Electric gained market share to begin with. Fuelled by VC money, the company figured out a distribution play, but it invested heavily in establishing manufacturing facilities, which will pay off only in the next three to four years.

lockquote>

The company reduced the valuation that it sought in the IPO, but the general view is that even this lower valuation was bloated.

As a public company, Ola Electric now faces the two-headed beast — the heavy losses and the drop in EV registrations amid customer complaints.

These twin factors have brought its share price close to its listing price, after a big boom soon after the stock market debut. Ola Electric listed at INR 75.99 in early August, and its share price more than doubled to INR 157.53 within a few weeks. While some profit booking can be expected during the festive season, this may not be the case with a new stock such as Ola Electric.

Having said that, the stock is now close to the listing price as of this week and ended Monday’s (November 4) trading session at INR 80.6 on the BSE.

And it’s unlikely that Aggarwal will be able to arrest this slide any time soon. Ola Electric no longer has the luxury of being a private company.

Plainly speaking, Ola Electric’s future hinges on two crucial factors — its ability to turn the narrative around in relation to the poor servicing and the lack of profitability, which is directly linked to the sales volume.

lockquote>

The company has bled market share through these past three months, and now there are renewed apprehensions that its path to profitability might be stretched.

So let’s answer the most pertinent question for investors and shareholders: when will Ola Electric snap its loss-making streak?

Ola Electric’s Breakeven Horizon

The public market’s aversion towards loss-making startups has been thoroughly discussed over the last two years. VC-backed giants such as Zomato, Paytm, Nykaa, Policybazaar and others were among the first few tech startups that took the hit.

The movement of their respective stock prices is directly linked to their profitability. But that didn’t deter Ola Electric from deciding to go public, even though the company did not have a clear outlook on profitability or break-even.

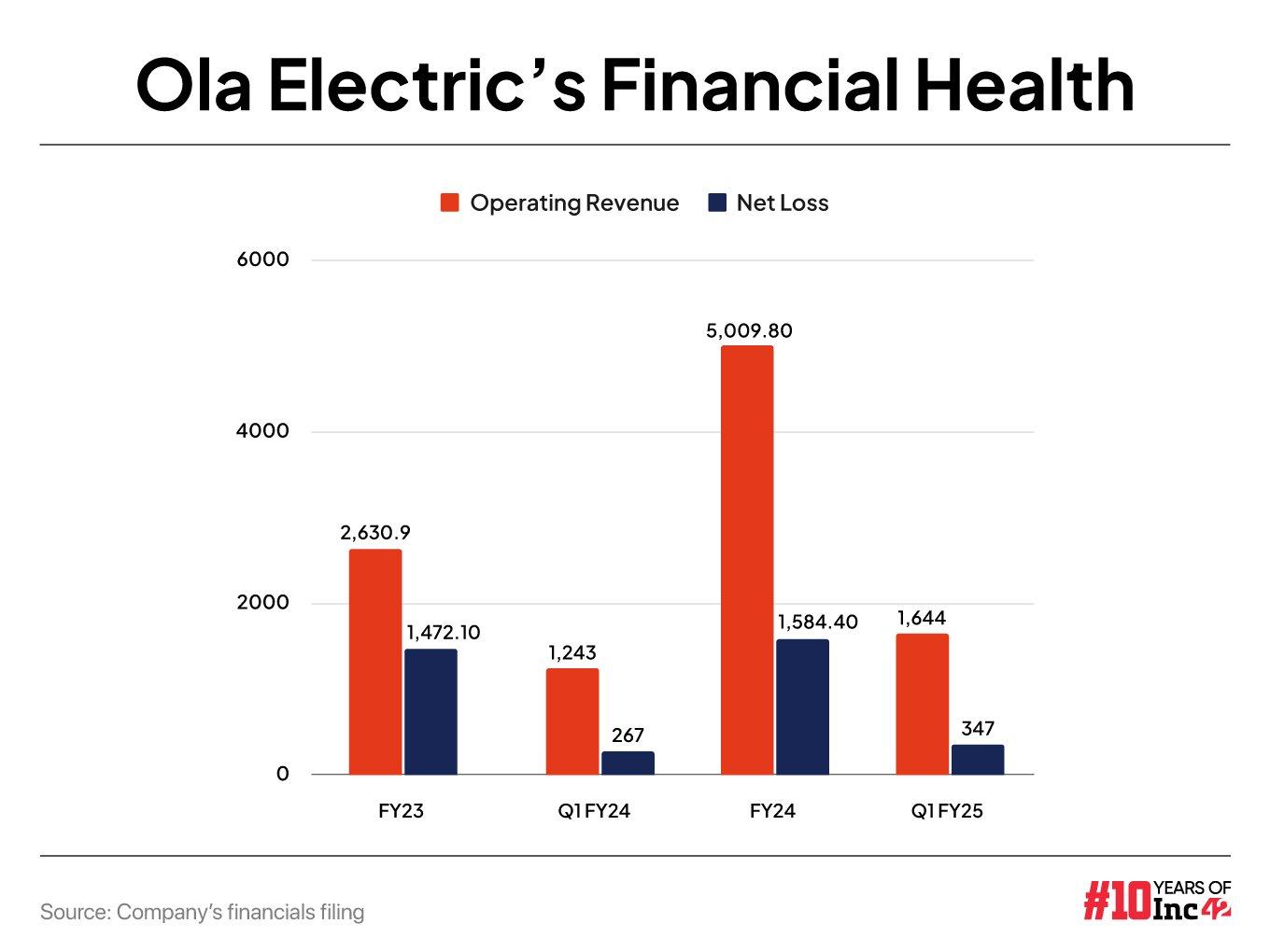

While Ola Electric has seen losses shrink and operating revenue grow QoQ from April to June 2024, this came as a result of a record number of scooter deliveries during the quarter.

It’s unlikely that Ola Electric would hit this peak again anytime soon. QoQ sales are expected to be currently volatile and impacted by factors including industry-wide trends such as festive season sales, discounts, and others. So one has to take the sequential growth figures with a healthy pinch of salt.

The noise around customer complaints and poor service quality has coincided with the festive season sales. Scooter sales are Ola Electric’s only source of operating revenue right now, and any dip in this metric will have a correlating impact on the income.

Ashwin Patil, senior research analyst at LKP Securities, told Inc42 that Ola Electric needs to focus on growing sales volume by about 30%-40% from the current levels to at least reach the breakeven mark.

Given the growth rate, it would take at least two to three years for the company to get out of the woods, Patil added.

lockquote>

BofA Global Research also sees Ola Electric getting to profitability only by FY27 at the earliest. Further, Goldman Sachs’ research note on Ola Electric estimates the company will remain loss-making on a consolidated level till FY27, or March 2027.

Even though the EBITDA margin is likely to improve from -25.3% in FY24 to -0.7% in FY27, Goldman Sachs’ projection is based on operating leverage arising from higher volumes, deflationary battery prices, and backward integration supporting the capital expenditure base.

lockquote>

But getting these ducks in the order will require a lot from Aggarwal and Ola Electric, and that’s not even accounting for new EV plays and models that might come up between now and 2027.

In Need Of An Image Makeover

With this distant outlook on profitability, there’s more caution being thrown in by brokerages and analysts. The priority, according to market observers, has to be the after-sales servicing.

Even a year or so before the IPO, Ola Electric had earned the unenviable reputation for poor service, with a few scooters catching fire and other build-related issues. Though these issues have been known for years, they have been swept under the carpet in pursuit of sales growth and market share.

In its research report, BofA added, “Ola Electric’s track record is limited to be sure of product quality. There have been incidents of scooter fire in the past and software issues. While it is a part and parcel of any nascent industry, any adverse word of mouth or lapses in service of the product can impact the demand from a mid- to long-term perspective.”

lockquote>

This gap was under fresh spotlight after the recent Twitter feud between CEO Aggarwal, and stand-up comedian and commentator Kunal Kamra. This led to more consumers bashing Ola Electric for product quality issues and servicing, and a show cause notice from the Central Consumer Protection Authority (CCPA).

Reportedly, the company has also brought in audit giant EY India for a “service transformation” in response to the public outcry.

LKP’s Patil added that for Ola Electric, the first priority is addressing its product quality. “Customers are extremely price and quality-sensitive. If news stories about its defective products continuously get published in the media, customers will definitely move to its competition’s products. This will keep delaying the company’s profitability trajectory.”

lockquote>

Can product diversification help in this scenario?

Some analysts are of the opinion that Ola Electric’s plans to penetrate into the electric three-wheeler segment could be beneficial for the company given it is a more profitable segment compared to two-wheelers. On the other hand, product diversification into electric motorcycles could also help the company gain more market share.

Ola Electric’s battery production ambitions remain another key variable in deciding its fate to improve fundamentals.

However, given the product and servicing-related issues, diversification might not be the best idea till these critical issues are fixed. “Ola Electric should focus on what they are doing at the moment rather than experimenting too much. Focusing on electric two-wheelers, which is its core competence, will help,” Patil added.

Ola Electric Vs Legacy OEMs

Not every industry works the same way, and hence, the path to profitability differs from company to company and from sector to sector.

In general, the auto industry is highly cost-intensive given the capex required to set up manufacturing facilities. However, at the moment, the cost of building an EV is comparatively lower than petrol or diesel (ICE) vehicles even despite the high battery costs.

EVs require fewer components, so comparing Ola’s trajectory to that of Bajaj or TVS who started as ICE OEMs wouldn’t be fair. The closest comparison is IPO-bound Ather Energy, which is also loss-making despite starting sales three years before Ola Electric. And as we noted there are differences in the positioning of both these homegrown EV companies, which makes the comparison.

Globally, we have an example in Tesla which took five years after production commenced to reach profits. But Tesla’s focus on the US market sets it apart from Ola Electric, besides the fact that it was heavily skewing towards the premium side of the car market unlike Ola.

Meanwhile, battery manufacturing might further delay Ola Electric’s profitability timeline as it is highly capex-intensive and operationally complex, with technology rapidly evolving in terms of battery chemistry and the charging vs swapping debate.

lockquote>

As per BofA analysts, Ola Electric’s battery manufacturing is a risk until execution is proven, given that procurement of raw material is still fraught with issues. Besides, there could be delays and cost overruns due to R&D when it comes battery manufacturing. As a result, the manufacturing process for new battery standards in the future could take significant time to reach perfection.

Goldman Sachs’ research showed that among the top six global battery manufacturers — CATL, LGES, BYD, Samsung SDI, Panasonic, and SK Innovation — the collective investment is more than $15 Bn over a 30-year period. Except for CATL and BYD, the other companies became profitable only three to four years ago.

These are challenges that one cannot hurdle with optimism alone; they require extensive planning and structuring of the ops. Ola Electric needs to clarify its stance on these issues if it has to convince shareholders and investors to continue showing faith.

lockquote>

In our look at Bhavish Aggarwal’s inner circle, we saw how the company has added leaders for each vertical and the battery manufacturing business is also part of this vertical integration push.

While market dynamics are beyond Ola Electric’s control, the consensus is clear – the company has to focus on the basics in the automobile industry to improve its reputation, which has a direct impact on sales and fundamentals.

One thing in Ola Electric’s favour is that the EV market is only going to grow every year, but capitalising on this to grow a profitable electric vehicle OEM is another matter altogether and unprecedented in the Indian context.

[Edited By Nikhil Subramaniam]