Rent keeps climbing while equity quietly compounds. If you’ll occupy at least 51 percent of the space, two SBA programs let you buy with only 10 percent down—far less than a typical bank note.

Government-backed loans for owner-occupied properties

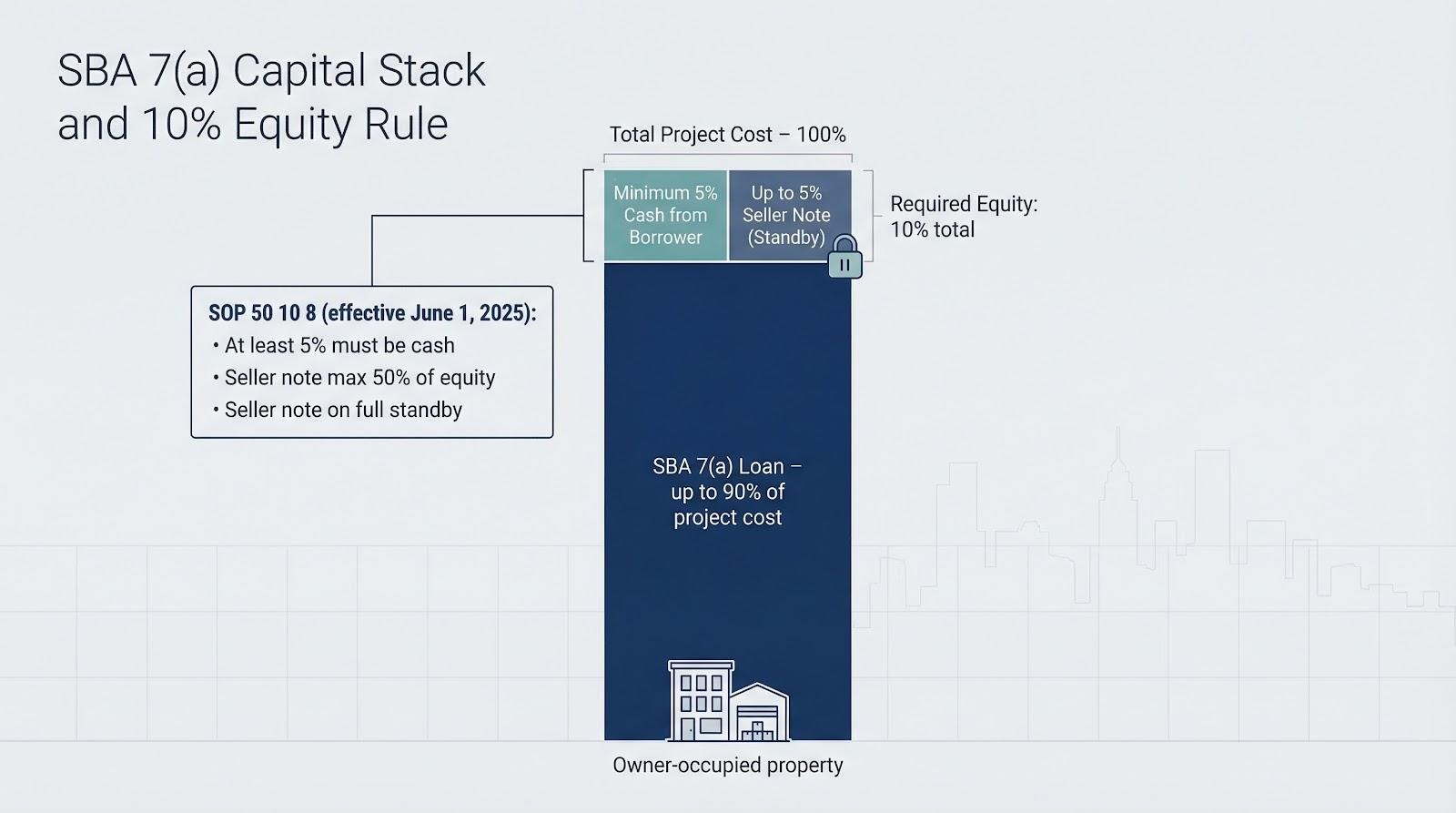

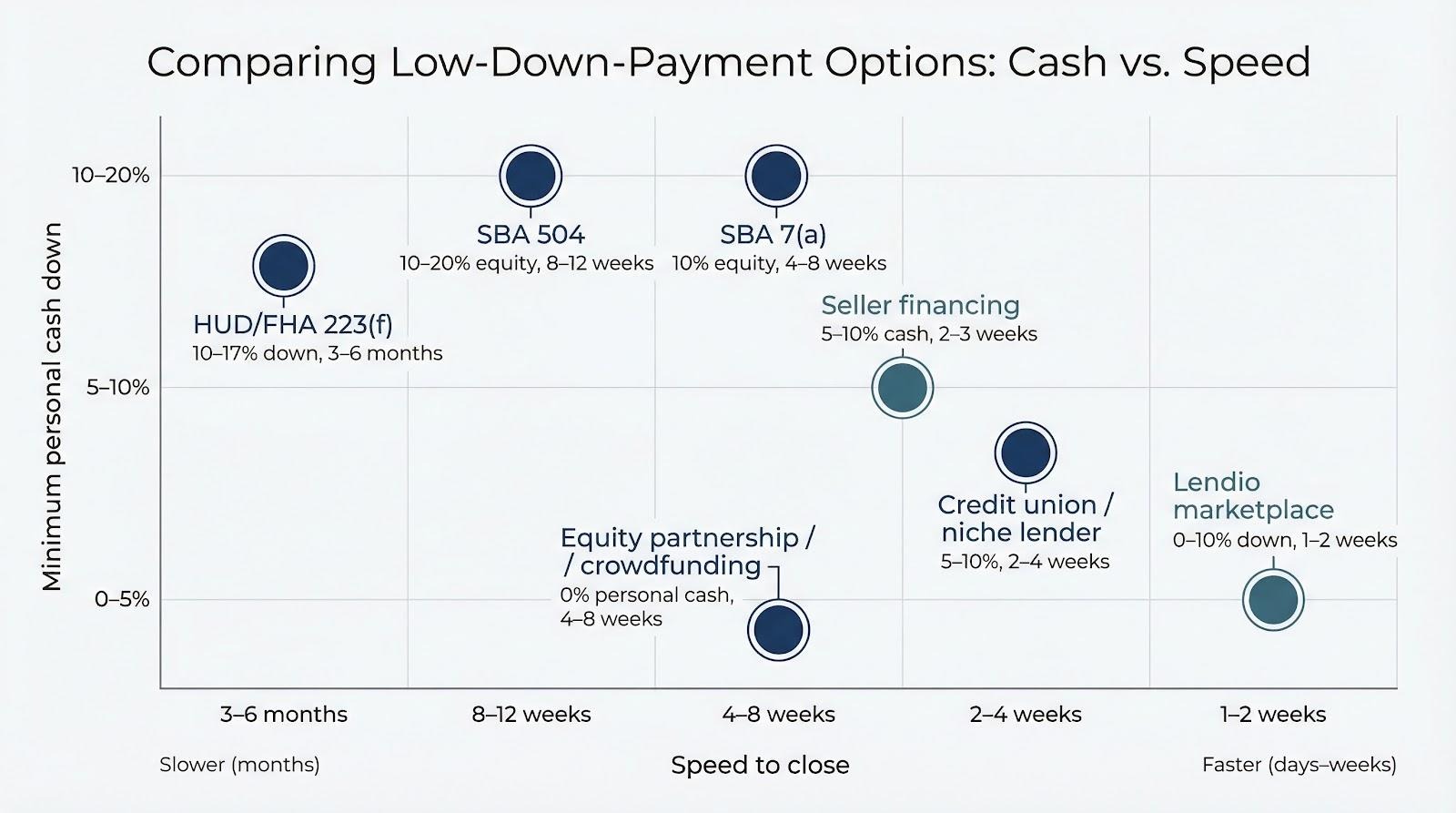

SBA 7(a) loan: 90 percent financing, one catch-all note

An SBA 7(a) loan is a government-guaranteed commercial mortgage that finances up to 90 percent of total project cost while also covering tenant improvements and working capital.

That 10 percent floor became non-negotiable on June 1, 2025, when SOP 50 10 8 took effect. The rule also capped seller carryback at half of the required equity and forced that note onto full standby—no payments—until the SBA debt is repaid (SBA down payment requirements). In plain English, you still wire at least 5 percent in real cash.

Rates hover at prime + 2.5–3.0 points, amortized over 25 years with no balloon. Lenders usually want mid-600 credit scores and a 1.25× projected debt-service coverage ratio, comforted by the SBA’s 75–85 percent guaranty.

Expect four to eight weeks of heavier paperwork than a straight bank loan. Still, for an owner-user with limited liquidity, 7(a) often lands where nothing else does: long amortization, low equity, and one payment that can even bundle furniture and working capital.

If you can wait a short time—and like paying roughly what you pay in rent—the 7(a) belongs on your shortlist.

SBA 504 loan: long-term fixed rate for hard assets

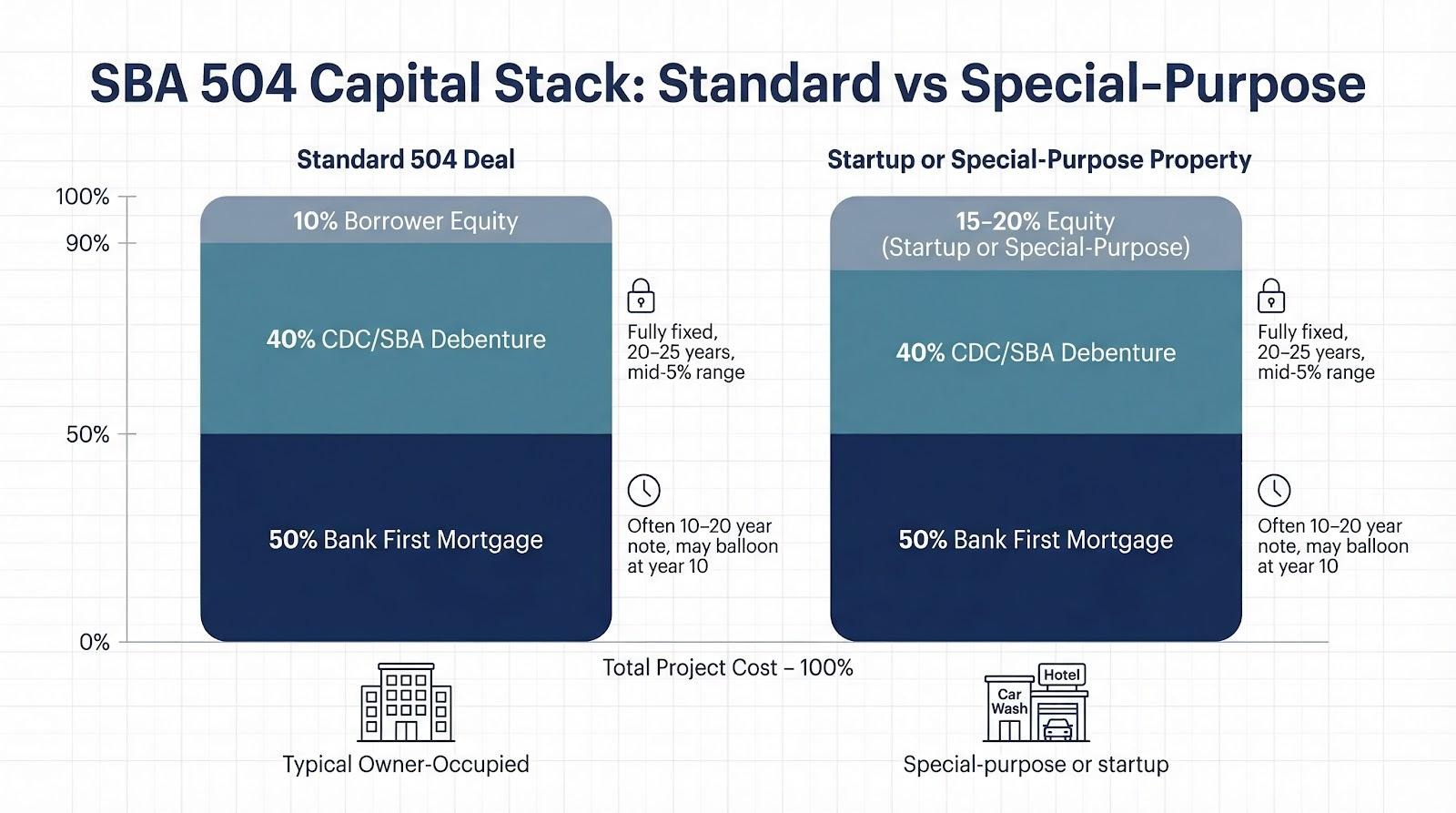

If the 7(a) is a Swiss-Army knife, the 504 loan is a laser-focused scalpel for real estate and heavy equipment.

A typical 504 stack looks like this: 50 percent first mortgage from your bank, 40 percent SBA-backed debenture via a Certified Development Company (CDC), and 10 percent borrower equity. According to Legal Clarity, your cash rises to 15–20 percent for startups (< 2 years) or special-purpose properties such as hotels or car washes.

The CDC slice is fully fixed for 20–25 years and currently sits in the mid-5 percent range. Blend that with a bank note that often balloons at year 10, and the overall payment usually beats rent while preserving capital.

Underwriters look for mid-600 credit scores, a 1.25× DSCR, and a plan to create one full-time job per $90,000 of debenture funds.

Closing takes longer—about 60–90 days with two lenders, two appraisals, and an SBA board meeting—but patient owners gain non-recourse on the CDC piece, low monthly payments, and the option to refinance existing real estate at up to 90 percent loan-to-value.

Bottom line: If you need a durable roof and can wait a couple of months, the 504 pairs fixed-rate certainty with the lowest cash requirement you’ll find outside a gift from grandparents.

High-leverage financing for multifamily investors

Apartment buildings follow their own playbook. Predictable rents and measurable occupancy let lenders treat them almost like bonds, opening the door to high leverage through HUD’s FHA 223(f) program.

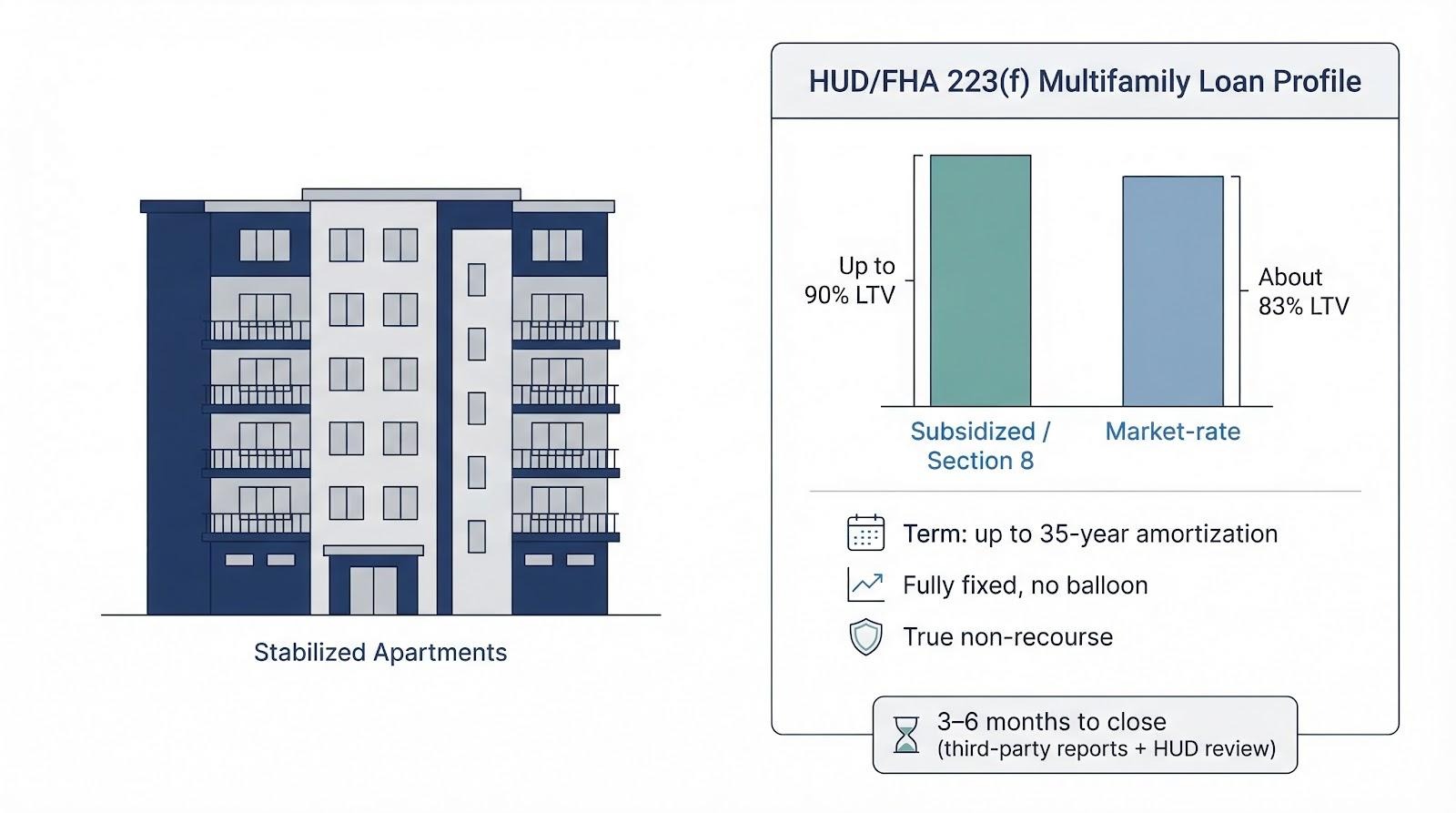

HUD/FHA 223(f): finance up to 90 percent of stabilized apartments

A HUD/FHA 223(f) loan is a government-insured mortgage that can cover up to 90 percent of value on Section 8 or other subsidized properties and about 83 percent on market-rate assets. According to Evergreen Capital Advisors, ten percent down on a $10 million complex leaves $1 million in reserve.

The loan’s wish-list terms include 35-year amortization, fully fixed interest, and true non-recourse. Because payments are spread over three and a half decades, the minimum debt-service coverage ratio can be as low as 1.11 on subsidized deals, a friendlier bar than most bank loans.

Time is the trade-off. Third-party reports, environmental reviews, and HUD’s queue often turn closing into a three- to six-month process. Scale matters, too; transactions below $5 million rarely pencil once fees are added.

Clear those hurdles and 223(f) locks in permanent financing before any value-add work begins, turning the loan into a capital-preservation tool that delivers steady cash flow without a refinance cliff. If your plan involves long holds and predictable income, few structures stretch equity as far.

Private-market and creative ways to shrink the check

Not every borrower fits a government mold. When timing is tight, credit is bruised, or you want to compare options without calling twenty banks, the private sphere rewards flexibility, speed, and negotiation.

Lendio online loan marketplace: one application, many 10 percent-down offers

Lendio is an online platform that submits a single application to more than seventy-five lenders and returns side-by-side quotes, often with down payments of ten percent or less. According to AZ Big Media, pre-qualification letters usually arrive within a day, letting you write an offer while competitors wait a week for a banker’s call.

Lendio Commercial Real Estate Loan Marketplace Screenshot

Because the marketplace is agnostic, you see rate spreads, fees, and amortization terms next to each other instead of tucked behind sales chatter.

Remember, Lendio matches you with a lender; it does not fund the loan. Final underwriting still lives inside the chosen institution, so have tax returns, rent rolls, and a polished business plan ready. Most documents overlap across lenders, so you answer diligence once instead of ten times.

For entrepreneurs who value time, transparency, and multiple low-down options, Lendio turns the lender hunt into an afternoon task rather than a three-month grind.

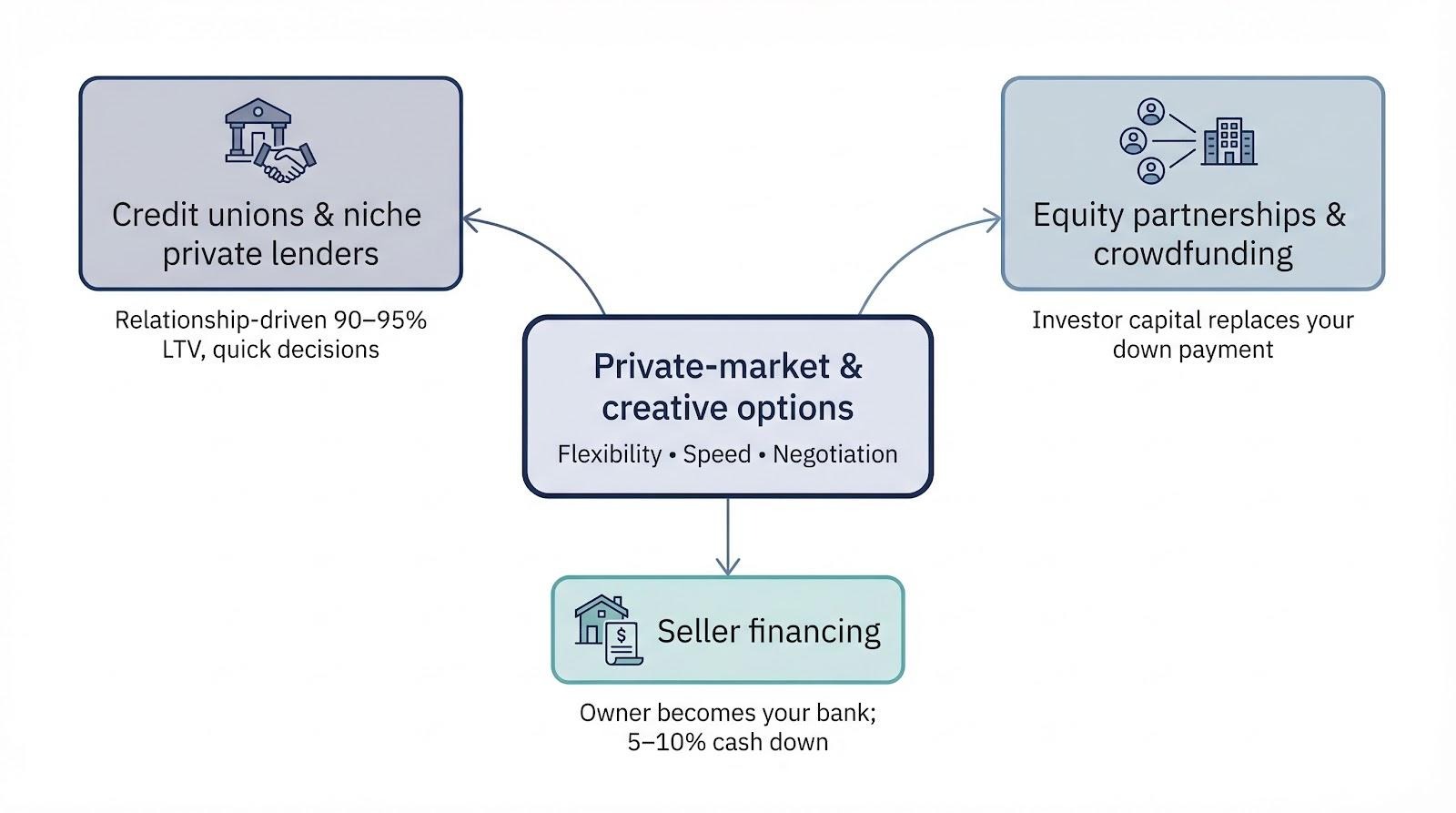

Credit unions and niche private lenders: relationship-driven 90 percent loans

Community lenders care more about your story than national averages. Long-standing depositors at a credit union, or sponsors known to a local debt fund, can sometimes land 90 to 95 percent loan-to-value mortgages with only a single-digit down payment.

Why the stretch? Smaller institutions prize full-relationship revenue: deposits, payroll, merchant services, even an IRA rollover. A low-equity real-estate note keeps everything in-house. Private lenders, meanwhile, chase yield; a slightly higher LTV at a slightly higher rate can beat Treasury returns.

Terms vary, so negotiate. Five- or seven-year fixed periods that reset or balloon, amortized over twenty to twenty-five years, are common. Rates range from prime plus 1.5 points for clean files to double digits if credit is rough. Lenders offset slim equity with stronger covenants such as 1.30× coverage, cross-collateral liens, or full personal guarantees.

Speed is the ace. A credit-union board meets weekly, and a debt fund can issue a term sheet in forty-eight hours and wire inside a month. For a quick close or a seller who dislikes federal red tape, that velocity can outweigh heavier guarantees.

These loans hide in plain sight. They rarely show up on comparison sites, and search ads seldom feature them. Ask your current banker about an “in-house exception window.” If you keep deposits and pay on time, the least stressful ten-percent-down offer might already be across the desk.

Seller financing: when the owner becomes your bank

Seller financing occurs when the current owner carries a note for most of the price, allowing you to put down as little as five to ten percent in cash.

Build trust first. Share your plan, personal financials, and a clear exit such as refinance or sale, and you can convert a seller into a lender who wants your success. Terms are flexible: interest-only periods, below-market rates, or five-year balloons that match a value-add timeline.

Everyone benefits. You conserve capital and skip bank covenants, while the seller defers taxes and earns interest without hunting for another investment. Both sides save on origination fees.

Risk lives in the balloon. Miss a payment and foreclosure is swift because the seller holds the deed. If you later pair a seller note with an SBA loan, remember the agency forces that note into full standby, so model cash flow accordingly.

Use seller financing for unique properties, tight deadlines, or balance sheets that still need seasoning. Retiring owners who favor passive income over lump-sum wires are ideal counter-parties.

Equity partnerships and crowdfunding: turning investors into your down payment

An equity partnership replaces the down payment with investor capital, shifting monthly obligations from fixed debt to performance-based returns.

Form an LLC that owns the property. Investors buy membership interests, usually for a preferred return plus a share of upside at refinance or sale. As managing member, you earn a promoted slice of profits for sourcing and operating the deal.

The appeal is clear: no personal cash leaves your bank account, and cash flow stays inside the project until it can pay investors. This cushion helps during lease-up delays or renovation overruns.

Crowdfunding platforms simplify the search for partners. They handle securities compliance, escrow, and investor dashboards, letting you focus on due diligence and execution. You give up more economics than with a single partner, but the capital pool widens.

Control is the trade-off. Outside money votes on major decisions, and exits can arrive sooner if investors need liquidity. Draft a business plan with clear milestones, distribution rules, and a target sale or refinance date. Transparency keeps everyone aligned and protects your reputation for the next raise.

Use partnership capital when upside potential outpaces what debt alone can unlock, such as ground-up construction or deep value-add plays. Done right, equity transforms a nice-to-have dream into a signed purchase contract.

Side-by-side comparison at a glance

The table below shows how each low-down-payment option trades cash today for cost, speed, or complexity tomorrow. Use it as a quick gut check before you call a lender or assemble partners.

| Program / Solution | Minimum cash down | Rate type & range | Term / Amortization | Recourse | Ideal borrower | Typical speed to close |

| SBA 7(a) | 10 percent (5 percent cash + 5 percent seller note allowed) | Variable, prime + 2.5–3.5 | Up to 25-year amortization, no balloon | Personal guarantee | Owner-occupier needing working capital too | 4–8 weeks |

| SBA 504 | 10 percent (15 percent for startups or special-purpose) | Bank: fixed or adjustable; CDC: long-term fixed about 5 percent | Bank note 10–20 years, CDC 20–25 years | Bank portion full recourse, CDC non-recourse | Owners seeking rock-bottom fixed payment | 8–12 weeks |

| HUD/FHA 223(f) | 10 percent subsidized, 17 percent market rate | Fully fixed, mid-5 percent range | Up to 35-year amortization, no balloon | Non-recourse | Multifamily investors, long-term hold | 3–6 months |

| Lendio marketplace | 0–10 percent, depends on matched lender | Varies by offer | 10–25-year amortization typical | Depends on lender | Borrowers who value speed and choice | 1–2 weeks (pre-qual in 24 hours) |

| Credit union / niche lender | 5–10 percent | Fixed early term, resets or balloons; 6–10 percent+ | 20–25-year amortization | Usually full recourse | Relationship borrowers needing quick close | 2–4 weeks |

| Seller financing | 5–10 percent (negotiated) | Highly flexible; often interest-only | 5–10-year balloon common | Property can be taken back | Buyers with rapport and solid plan | 2–3 weeks |

| Equity partnership / crowdfunding | 0 percent personal cash | No loan—equity return structure | Depends on operating agreement | Shared control | Sponsors with strong upside projects | 4–8 weeks (raise dependent) |

A table is a map, not the terrain. Rates change, lenders adjust guidelines, and partnership terms hinge on trust. Treat this snapshot as a starting point and confirm every detail with current term sheets.

Myths and FAQs about low-down-payment commercial loans

“Is zero-money-down real?”

Almost never. Lenders want real equity—cash, a fully deferred seller note, or outside capital. When a pitch claims one-hundred-percent financing, expect high interest, extra fees, or a short balloon.

“Can I sidestep the SBA ten percent rule?”

No. SOP 50 10 8, effective June 1, 2025, sets the equity floor at ten percent and limits how much may come from a standby seller note. Files that ignore the rule get declined.

“What if I borrow my down payment?”

That additional loan appears in your global cash-flow test. Banks still require a 1.25× coverage ratio after counting the new payment, and the borrowed funds cannot be secured by business assets already pledged.

“Does seller financing always avoid guarantees?”

The opposite. Sellers usually demand a personal guarantee or extra collateral because their note sits behind the senior lender. Treat their paper with the same respect you give a bank.

“Are HUD 223(f) loans only for massive developers?”

Deals below five to seven million dollars rarely justify the third-party report costs, yet regional investors who syndicate equity close 223(f) loans every year.

“Why do credit unions ask for higher DSCR if they lend ninety percent?”

Leverage and cash flow move in opposite directions. A higher coverage ratio offsets the thinner equity cushion and reassures the credit committee that one vacancy will not disrupt payments.

Conclusion

Every path in this guide trades a different resource for lower upfront cash. SBA 7(a) and 504 loans offer government-backed stability at 10 percent down for owner-occupiers, while HUD 223(f) stretches equity furthest on stabilized apartments. When speed or flexibility matters more than federal guarantees, Lendio’s marketplace, credit-union relationships, seller financing, and equity partnerships each fill the gap. Line up your timeline, coverage ratio, and risk tolerance side by side, confirm current terms with each lender, and move before rising rents outpace the closing calendar.