There’s optimism within Paytm![]() again. In fact, founder and CEO Vijay Shekhar Sharma said the Q1 FY25 results mark the end of tough times for the Indian fintech giant.

again. In fact, founder and CEO Vijay Shekhar Sharma said the Q1 FY25 results mark the end of tough times for the Indian fintech giant.

Sharma lauded the company’s resilience and the capability of Paytm’s products, and said now the target is to head towards profitability in this fiscal year. This bullishness is not unwarranted, but there is still a long way to go before Paytm is back to where it was even three quarters ago.

One year ago, we said Paytm was knocking on profitability’s doors, and the momentum definitely seemed to be carrying the company towards this milestone after the bloodbath on the stock market post listing. However, since then, it has been a season of adjustments, reassessment, scaling back and preparing the Paytm machinery for leaner times.

After the Q1 results, it’s clear that Paytm has taken some steps forward, but there is a lot more of the mountain left to climb for Sharma and Co. This Sunday, we are looking to bring more context to Paytm’s Q1 results, in light of what’s happening in the market.

But as usual, a look at the top stories from our newsroom this week:

- Shein’s Second Innings: Shein is back in India with a little help from Reliance Retail, but can the fast fashion behemoth recreate the magic that worked for it in India before the ban in 2020?

- BYJU’S Vs Bankruptcy: After months of speculation, BYJU’S was finally hit with insolvency proceedings this week, and the company is precariously close to being auctioned for its parts as creditors look to settle matters

- Looking Ahead To The Budget: While most Indians would welcome tax rate cuts with open arms, the Union Budget 2024 need to look at long-term measures to boost consumer spending and the Indian startup story

Where Paytm Stands After Q1

Much of Paytm’s optimism at the end of Q1 stems from the fact that new merchant signups are reaching January 2024 levels and there has been an increase in payments GMV — both are critical indicators of the health of the company. Merchant stickiness is more important than consumer stickiness for Paytm, given the better unit economics on the merchant side and the ability to continually cross-sell products.

There was only a marginal increase in the merchant subscriber base to 1.09 Cr, but daily merchant payment GMV (excluding discontinued products) went back to January 2024 levels, much before the downturn began.

CEO Sharma claimed that this is the beginning of the end of the tough times. “This quarter reflects the full impact of the challenges we faced. As a team, we are committed to navigating through these times with a focus on compliance. My team and I are committed to ensuring we return to profitable quarters,” Sharma said.

But this optimism hides just how much more climbing Paytm has to do.

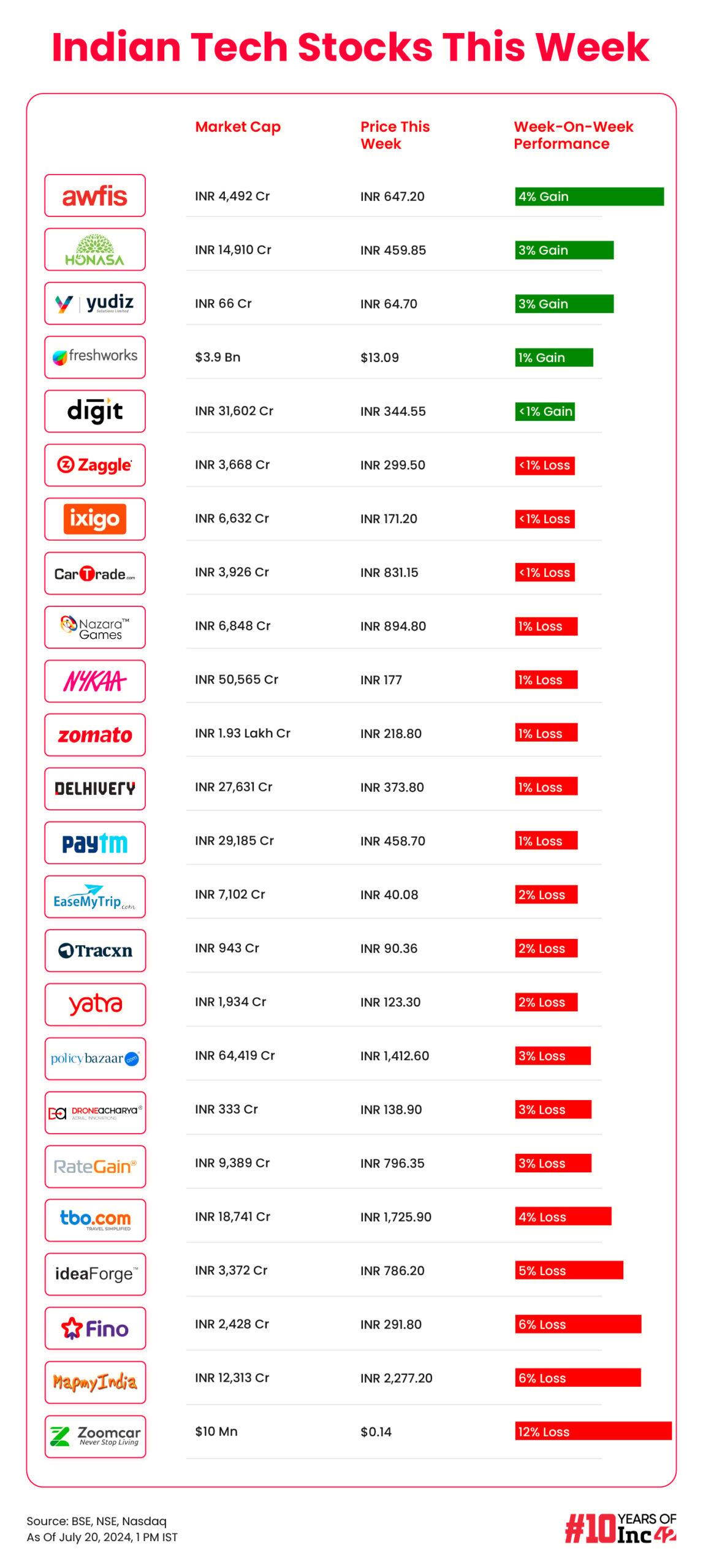

— Paytm reported a net loss of INR 840.1 Cr, more than double quarter-on-quarter

— Operating revenue fell by 36% QoQ to INR 1,502 Cr

— Plus, revenue from financial services (loans primarily) was down by 8% to INR 280 Cr

On personal loans, Paytm’s focus is on the distribution side and the company is looking to add more bank and non-bank partners to diversify its revenue streams. This particular change and the retreat from lower ticket size loans has nearly halved the revenue from financial services.

In other words, Paytm is not completely out of the weeds.

The Uphill Climb Continues

For one, Paytm has not exactly cut down on all expenses. While employee costs have lowered as a result of layoffs, there’s a lot more that needs to be done.

The scale of the potential layoffs and restructuring can be understood by the fact that Paytm reported just over 31K employees in the sales team as of Q1 FY25, which is down from 35K employees in Q4 FY24. In three months, the company has let go of nearly 5K employees from the sales team, but this is a drop in the bucket when considering Paytm’s target of saving INR 500 Cr in employee costs in FY25.

In Q1 FY25, indirect expenses (excluding ESOP costs) rose to INR 1,301 Cr from INR 1,186 Cr in the previous quarter and INR 1,220 Cr last June.

Even though employee cost has come down by 9% QoQ, it is still higher on a YoY basis. “Given the focus on merchant acquisition, we will continue to invest in the sales team while having a higher focus on productivity of sales employees,” Paytm said.

Further, marketing costs were also higher during the quarter since the company had to spend heavily to communicate the changes to its platforms after the RBI action. “Cost-optimisation across the board will continue to be our key focus area and we will continue to be disciplined about our overall cost structure.”

During the analyst call on Saturday (July 20), Paytm CFO Madhur Deora said that employee costs will go down 5%-7% quarter-on-quarter. He added that the marketing expenses were higher during the June quarter because of new ad campaigns but should go down in the coming quarters as marketing activities are scaled back.

Another big challenge for Paytm is that it still cannot bring on new users for UPI payments. Given that Sharma said the next few quarters will see a bigger push on the payments front to become a cross-selling channel, changing this will be crucial for Paytm’s future growth.

“In the process of completing technology and consumer migration. The merchant migration is completed, but on the consumer side, it is a multi-bank system, so all banks have to participate and our primary partner YES Bank has to also expand on certain technologies. We’re at the tail end of the migration on the consumer side and we can go back to the NPCI to request to add new users,” Sharma said.

Jio-Sized Threat For Paytm & Co

Of course, the competition is watching Paytm and many rival payments platforms are grabbing users and retaining them with new loyalty programmes and other cross-selling. Even Flipkart has jumped into the payments game and is investing heavily to grab and retain users.

And let’s not forget Jio Financial Services (JFS), which is expected to go from beta to full launch in the next quarter. JFS is essentially doing everything that Paytm was doing before the RBI action disrupted the momentum.

More entrenched players like PhonePe and Google Pay have cashed in on the vacuum left behind by Paytm, migrating its users to other banks and nodal accounts. Now, Paytm not only has to spend to get these merchants back and retain them but also compete in the cross-selling of financial services to these merchants.

But, as we said in the beginning, Sharma is optimistic and confident of beating the odds. Earlier this month, the company’s CEO said that RBI action and the fallout did take a heavy toll on his emotional and personal wellbeing, though it wasn’t the worst moment in Paytm’s 14-year journey.

“At a professional level, I would say we should have done better, there is no secret about it. We should have understood the situation better. We had responsibilities which we should have fulfilled in a better way. I think we have learnt our lesson from the issue and are making a better comeback,” Sharma said at an event in Delhi.

Despite that setback, Sharma said his vision continues to make Paytm a $100 Bn company. At the moment, that seems like a pipe dream; for now Paytm has to get back to the growth seen till January. And that will take a lot more from Sharma and the fintech giant.

Sunday Roundup: Tech Stocks, Startup Funding & More

- Reliance Retail’s digital and new commerce businesses contributed 18% to the total revenue of the retail giant in Q1 FY25, while ecommerce platform JioMart saw average bill value grow 16% YoY

- Several states, including New Delhi, Karnataka, Tamil Nadu, Goa, and Kerala, are said to be exploring allowing alcohol delivery through Swiggy, BigBasket, Zomato, and other platforms

- Ola Electric is likely to be valued at around $4.5 Bn for its upcoming IPO, a decline of roughly 20% from its last private valuation, according to reports this week

Disclaimer

We strive to uphold the highest ethical standards in all of our reporting and coverage. We StartupNews.fyi want to be transparent with our readers about any potential conflicts of interest that may arise in our work. It’s possible that some of the investors we feature may have connections to other businesses, including competitors or companies we write about. However, we want to assure our readers that this will not have any impact on the integrity or impartiality of our reporting. We are committed to delivering accurate, unbiased news and information to our audience, and we will continue to uphold our ethics and principles in all of our work. Thank you for your trust and support.