The venture capital industry, both at home and abroad, has encountered stiff challenges in the past couple of years. The media has been abuzz with the departures of longtime VCs at the top and the transformational rebranding of storied funds (Peak XV Partners, Elevation Capital).

Then again, global headwinds have deterred limited partners (LPs) from loosening their purse strings while cash burns and profitability issues have plagued many renowned portfolio companies, stuff that headlines are made of.

Nevertheless, there are steady players like Chiratae Ventures (formerly IDG Ventures India), an India-focussed VC veteran that has been operating since 2006. It started as a small team of seven but has grown to 30+ members, with $1.2 Bn under advisory. To date, it has made 50+ exits, including three IPOs by Newgen Software, Policybazaar and Yatra.com.

Globally, venture capital could be at a tipping point with investors like Reid Hoffman, Michael Moritz, Jeff Jordan and their ilk stepping back and several VC firms cutting their fund-raising targets. Three months ago, the Foundry Group, a Boulder-based VC that has backed 200+ startups since 2006, said it would no longer raise new funds.

Not so with Chiratae.

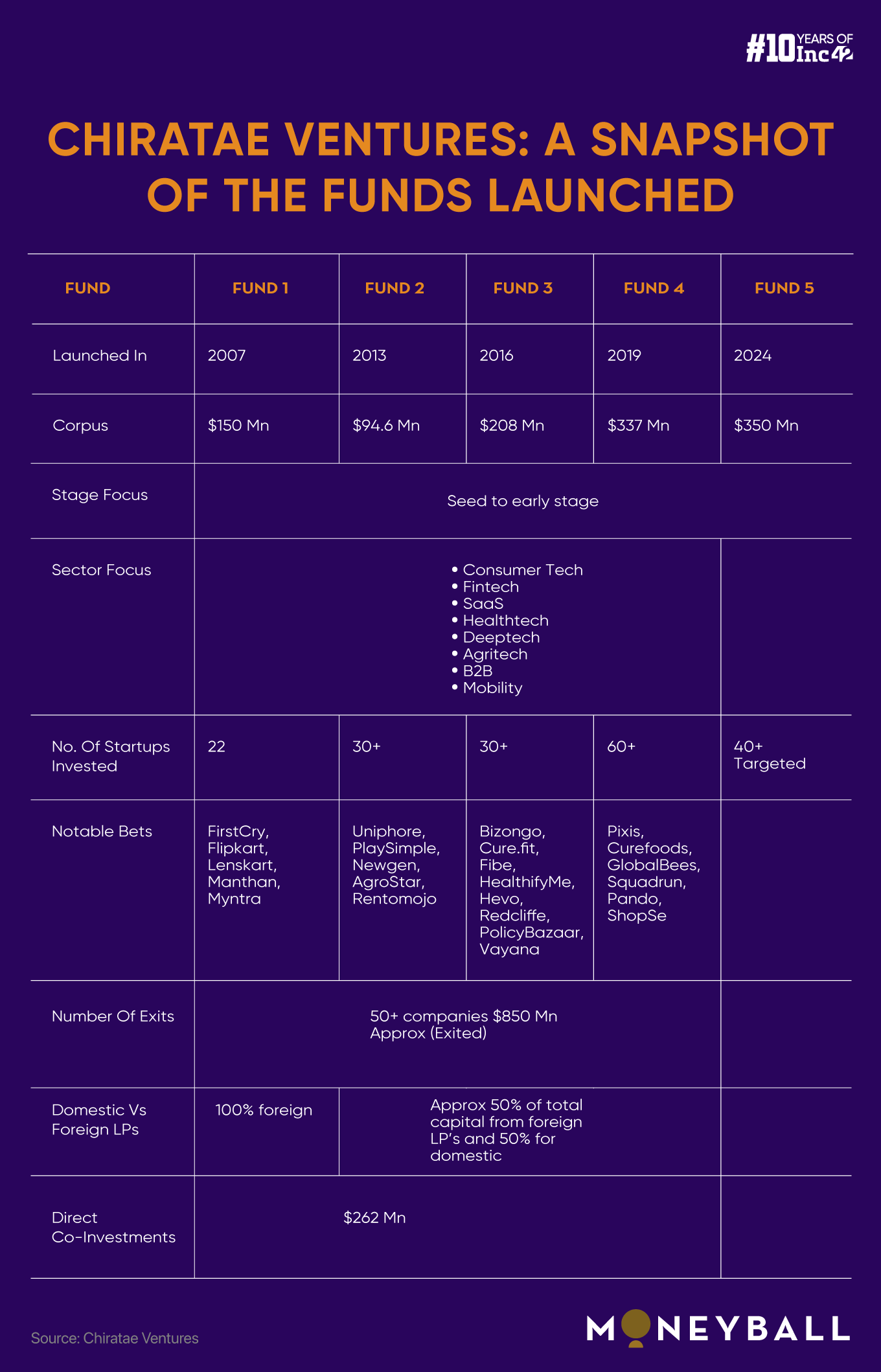

Even when the going got incredibly tough last year (2023) due to a funding winter globally, it announced the final close of its maiden growth fund in May 2023. The fund was oversubscribed by 34% and the total corpus amounted to INR 1,001 Cr (nearly $120 Mn), although the initial target was INR 750 Cr ($90 Mn).

The VC firm’s global advisory board includes industry veterans such as Ratan Tata (chairman emeritus, Tata Sons); Infosys cofounder Kris Gopalakrishnan; Asian Paints’ vice-chairman Manish Choksi; Bruno Raschle, founder of the Zurich-based Adveq Group; Andreas Hettich, chairman of Germany-based Hettich Corporation.

Regional Advisory is comprised of Ken Shibusawa (Japan), Founder and CEO of &Capital, Senior Advisor at Brunswick Grp; Pat McGovern III(USA), Trustee and chair of the Investment Committee at McGovern Foundation; Puneet Pushkarna (Singapore) GP at solmark.com and Chairman of TiE -SG; and Dr Ferzaan, Engineer, Cofounder and Chairman of Cytecare Hospitals (India).

The success story was initially scripted by founders Sudhir Sethi and TCM Sundaram, who have known each other for more than 30 years. Interestingly, from 1996 onwards, they recognised a big opportunity brewing across the Indian startup landscape, even though it was a nascent ecosystem at the time.

lockquote>

For context, India saw the emergence of its first homegrown portal Rediff.com, its first local search engine JustDial featuring B2C and B2B SME listings and its first ecommerce company Fabmart between 1996 and 1999.

As the ecosystem grew and young ventures started attracting private investments, Sethi and Sundaram roped in Ranjith Menon into the team in 2007. Ranjith subsequently became a partner. It was a great value addition as Menon had worked at the intersection of engineering (mechanical), electronics and software, bringing to the team his unique expertise and perspective needed for identifying emerging sectors at the time.

Myntra is one of Chiratae’s early bets, which Sudhir identified, and invested in. Ranjith supported Sudhir in this deal. Chiratae rolled over its investment in Myntra to Flipkart and subsequently sold its Flipkart stake at the time of Walmart’s purchase.

In 2011, Venkatesh Peddi joined the team and subsequently became a partner and managing director, bringing a deeper sector focus across the key themes Chiratae has been following. He also supported TCM in his investment in Lenskart (still in its early days) to the VC fund’s portfolio. Six years later, the eyewear brand entered the unicorn club and is currently valued at $4.5 Bn.

Despite cyclical downturns and the changing nature of the VC business – many are now getting into wealth management and investment advisory to broaden their scope – Chiratae has had a smooth sail most of the time.

It boasts a portfolio of 130+ companies, including eight unicorns like– Cult.fit (earlier Cure.fit), FirstCry, Flipkart, GlobalBees, Lenskart, Policybazaar, MyGlamm (now Good Glamm Group), and Uniphore. It also claims a steady track record of returning capital to investors every year over the last 12 years.

As part of Inc42’s Moneyball series, we had long talks with Chiratae’s founders, as well as two partners, Menon and Peddi, to take a trip down memory lane and get an insight into how the fund was set up, its key learning, exit strategies and the journey ahead.

lockquote>

A Camaraderie That Cemented A Venture Capital Foundation

Long before they entered the world of venture capital, Sethi and Sundaram worked together at Wipro’s Bengaluru office in 1986-87. They soon became good friends and have got along ever since. Sethi left Wipro a decade later to join a global VC fund, Walden International, as its India head. Sundaram joined the fund in 1999 and they led the business together.

Venture capital was becoming a popular concept by then and quite successful in countries like the US. The duo believed it would be successful in India, too, although there were few takers at the time.

“Working for Walden at that time was a learning experience. It was a very small world, but that’s where we learnt the ropes. One of the biggest takeaways was that the venture space and the landscape for building new technology companies were vast,” said Sethi.

For instance, several funds, such as SAIF Partners (now Elevation Capital), Norwest Venture Partners and Aavishkaar Capital, were operational in the country.

In 2006, Sethi and Sundaram raised an anchor investment from IDG USA to set up a $150 Mn India-focussed VC fund called IDG Ventures India. However, after the death of Patrick J. McGovern, the founder-chairman of the IDG Group, the VC firm was rebranded as Chiratae Ventures in 2018.

“Chiratae means leopard in Kannada. It highlights another passion of Team Chiratae, as a few of us are wildlife photographers. Our passions have gelled well in our launch video and it is mesmerising,” chuckled Sethi.

lockquote>

Why Chiratae Got Bullish On An LP Base From India After Fund I

Chiratae Ventures has been operational for more than 17 years. But when the founders and other partners started working on their first fund, little did they know what it would take to make it happen. For example, they had to learn how to raise capital in the first place.

Recalling Fund I, Menon said that Chiratae (then IDG Ventures India) had 100% offshore capital on the LP side. However, IDG USA had significant R&D capital at the time, which got the VC firm thinking whether domestic capital could play a pivotal role in building India’s startup ecosystem.

That was why it was determined to evangelise startups as an asset class in the domestic market while raising Fund II.

“It was quite difficult because not many people understood the associated risk. Entering a VC fund as a limited partner means putting in patient capital for eight to 10 years with no guarantee of returns. So, we spent a lot of time on building confidence in this asset class,” Menon added.

lockquote>

Their efforts paid off. As Sethi claimed, 20% of its Fund II was Indian rupee capital and Chiratae was the pioneer in that space.

“Today, we have an AUM of about $1.2 Bn, including INR 4,000 Cr in domestic capital. It also makes us the single-largest fundraiser in the country across the VC space. We are raising Venture Fund V right now,” said Sethi.

What Drives ROI, Startup Growth: 4 Key Performance Areas Chiratae Looks At

For Chiratae, it is strategically important to examine every company, entire sector and even market/sector outlook for 10 years to identify white spaces and fundable startups.

“After identifying those white spaces, we look at the companies and decide which has the stellar team and which has the differentiated strategy. We can get the best outcome when they align with a large market opportunity,” said Sundaram.

Also, it is essential to determine whether companies are solving real-world problems and creating large-scale impact. For example, Lenskart is an eyewear brand for everyone. But Chiratae saw it as a company solving the problem of myopia and similar medical conditions for 2 Mn people worldwide, making it a massive market.

Chiratae has created differentiated outcomes because of this approach and it continues to look for investible white spaces/verticals. Take, for instance, vertical ecommerce. There was a time when everybody wanted to back horizontal ecommerce companies like Flipkart and Snapdeal. In contrast, Chiratae invested in several vertical ecommerce ventures like Myntra, Lenskart and FirstCry. All of them are market leaders today.

“That is something we have done differently. We have been investors in that sector [ecommerce] since our first fund. In fact, it has been an important, strategic sector for almost all our funds. That [exposure] made us stand out from the rest, and entrepreneurs came to us whenever they had the choice to decide whom they wanted to raise money from,” said Sundaram.

lockquote>

How The Investment Thesis Has Evolved At Chiratae

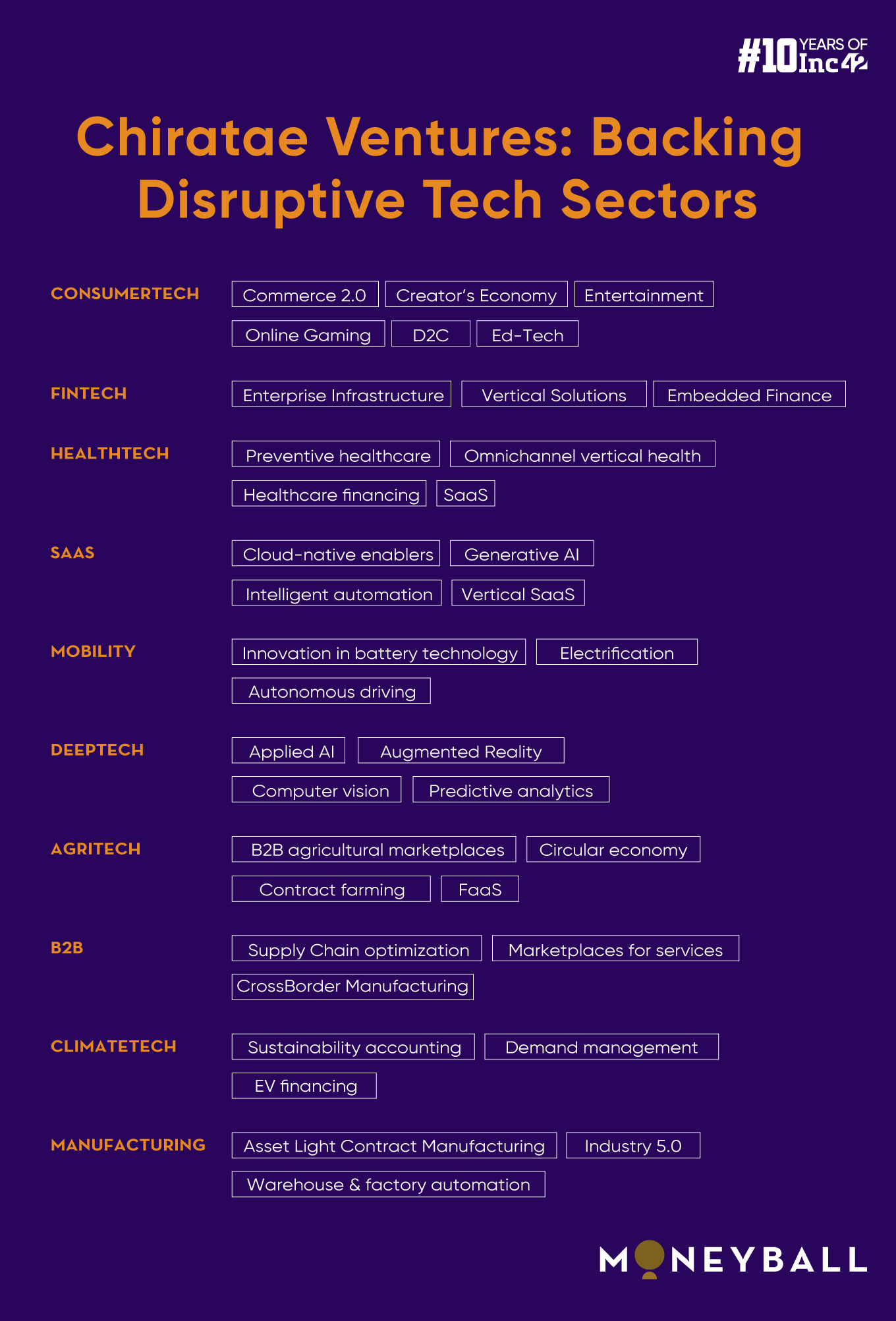

Chiratae’s focus areas for Fund I included software (SaaS was not a popular industry term at the time), hardware (manufacturing) and ecommerce. But with each new fund, the VC firm’s sector focus has deepened.

The broad areas attracting investments include consumertech, fintech, healthtech and SaaS (software as a service). However, the VC firm has continuously evolved, adding new and emerging sectors as these verticals become more extensive and critical. As of now, Chiratae is looking at mobility, deeptech, climate tech, gaming, DevOps, generative AI (genAI) and other current trends.

“We have an active thesis on these and other large verticals that we have seen from the past, whether it is fintech, SaaS or consumertech and healthtech,” said Peddi. “We see more and more subsegments emerge, and we plan to go after these as new sectors going forward. Moreover, we will keep evolving and continually adapt to changing trends as new opportunities arise within these segments.”

Recalling the fund’s early days, Peddi clarified how its investment strategy changed over the years.

“In the first five years, it was a lot more generalistic – we focussed on companies that could grow quickly using technology,” he added. “In the next five, it started getting deeper and became more specialised from a sector perspective and region-wise. Also, winners from the previous cycle began to emerge. That was exciting.”

lockquote>

The Chiratae team also realised that technology is critical in building differentiation and ensuring robust returns. Tech disruption enables massive scale, low-cost market penetration and a higher target/addressable market. It also helps create a very different moat around the business through innovative products/services. Eventually, these ventures could fend off competition and become large companies.

As Fresh Blood Comes In, Investors Need To Act As Mentors & Trusted Partners

Chiratae primarily invests in companies where everything is new, including the business model, revenue model, technology and the go-to-market strategy. The average age of the entrepreneurs with whom it is working is around 20s. There is no set playbook to replicate, and founders are not very experienced, thus putting the onus on investors for successful outcomes.

Sethi believes that investors have to prove every day their capability to sit on the boards of their portfolio companies. They have to learn about the company, the sector, products/services, the technology, the team and more so that they can help the startup through their networks within and outside the organisation.

He also thinks that the day capital goes into a company, the VCs have to be very humble about it. Building a company is a lonely and complex sequence of things and a trusted partner is needed to go the long mile with the entrepreneur.

“We are constantly trying to position ourselves as a trusted partner and mentor to entrepreneurs. Moreover, entrepreneurs today do their due diligence regarding investors before raising funds. Therefore, investors have to stay ahead of the curve. More importantly, everything we do must be better than what we have done before,” added Sethi.

lockquote>

Reaping The Gains: Will Dragons Deliver Big Returns?

Chiratae believes building deep exit capabilities is critical for any venture capital fund. But rather than cash-guzzling unicorns, a fund should have ‘dragons’ in its portfolio to achieve that. For context, dragons are early-stage startups that keep costs under control, go for sustainable growth and may return the entire fund amount. Unsurprisingly, dragon startups can raise $1 Bn or more in a single round, given the kind of returns that may happen.

The VC firm did not reveal much regarding portfolio sale, but Sundaram provided some interesting numbers. “Chiratae has done 50+ exits out of the 134 portfolio companies. And its highest exit saw nearly 43x returns,” he claimed.

lockquote>

According to the founders, they have attempted to develop a disciplined approach to exits, a key reason why they are able to return $846 Mn in 12 years from 2012 onwards.

Sundaram emphasises that exits don’t happen on their own. They require careful planning because it may take six to 18 months after the founders decide to sell. It is also essential to maintain transparent communication with founders about exit plans and work closely with them, the board and co-investors.

As exit looms, there could be differences of opinion and investors need to be sensitive about these. But it makes a lot of difference as long as one can keep the guardrails together and move towards the final goal.

According to Sethi, VCs should prepare for massive exits translating into huge gains. At the macro and company levels, startups are growing much faster and good exits can happen soon if things are done right from the beginning. As VCs focus on overall execution, they should ensure proper governance, onboard the right people and have the right investors on the cap table so that the company has the capital to grow.

“VCs should also talk to potential buyers to find a good home for the business [and the founders, in case they choose to stay for some time]. When a company is sold, it is not the end but the beginning of a new chapter, and everything should work out well,” he added.

lockquote>

Chiratae’s Learning Along The Way & The Road Ahead

“Throughout the journey, we have pursued scale and performance, adding product lines to optimise achievements and fine-tuning our exits. In 2024, we are poised to become the first fund in India to cross $1 Bn in exits,” claimed Sethi.

Going forward, Chiratae is excited about the opportunity to grow companies and technologies at the global level.

Unlike in the early 1990s, when Indian ventures looked to the US to replicate their business models, innovation in India has now reached global standards, said Sundaram. “It is not just about problem-solving but also impacting global markets. India is no longer seen as a leader in emerging markets, confined to building there. Today, innovative startups like Pixis and Miko are solving problems in the US and the EU. They are on an equal footing with their global counterparts.”

For the curious, Pixis is a no-code AI platform that helps brands optimise and monitor marketing campaigns for effective outcomes. On the other hand, Miko develops an AI-based companion robot to educate and entertain children globally.

Founders and partners at Chiratae Ventures firmly believe that the growth of the Indian startup ecosystem hinges on raising new funds, better availability of domestic capital and the rise of unique products and services through innovation and technology edge. And the focus should be on nurturing the startup ecosystem as a whole.

Talking numbers, Sundaram said India’s GDP could reach $20 Tn to $35 Tn by 2047 when the country celebrates its 100th year of Independence.

“It is a once-in-a-lifetime opportunity to grow from the current GDP of $3.5 Tn to a six-times scale. And it will be substantial as technology disrupts across the ecosystem, whether it is banking, investing, lending, manufacturing, or all the new-age media or next-gen AI that is going to come. We are excited about this opportunity and the scope to back entrepreneurs in their 20s who are fearless about taking on the best in the world,” he concluded.

lockquote>

[Edited by Sanghamitra Mandal]

Disclaimer

We strive to uphold the highest ethical standards in all of our reporting and coverage. We StartupNews.fyi want to be transparent with our readers about any potential conflicts of interest that may arise in our work. It’s possible that some of the investors we feature may have connections to other businesses, including competitors or companies we write about. However, we want to assure our readers that this will not have any impact on the integrity or impartiality of our reporting. We are committed to delivering accurate, unbiased news and information to our audience, and we will continue to uphold our ethics and principles in all of our work. Thank you for your trust and support.