Mohit Gulati, cofounder of Altius Venture Partners, angel network Oliphans Capital and ITI Growth Opportunities Fund (he is also the managing partner of ITI GO), believes in the power of purpose, the raison d’être, to be precise. He may not have been the brightest student as a kid, but he was a dreamer with an in-depth understanding of people’s aspirations. Growing up with doctor parents, he also understood the importance of performance and delivery.

Given this mindset, Gulati wanted founders to succeed and knew he must become a jack of all trades to help people with different aspirations. This philosophy is also reflected in his work at ITI GO.

An MBA from IIT-Bombay and an alum of the University of Pennsylvania, he launched Fund I worth INR 62 Cr in 2018 in partnership with the Investment Trust of India (ITI). The financial services conglomerate is led by Sudhir V. Valia, cofounder and director of Sun Pharma, and owns more than 15 businesses in key sectors such as lending, broking, wealth management and more. As a result, the group provides significant cross-synergies for ITI GO across various verticals, including equity funding, venture, debt, investment banking and IPOs.

The fund has performed well in the past five years, investing in 22 startups and returning half the capital to investors. Gulati is working on his next endeavour, ITI Growth Opportunities Fund![]() II, which has a corpus of INR 200 Cr and a greenshoe option of INR 100 Cr.

II, which has a corpus of INR 200 Cr and a greenshoe option of INR 100 Cr.

“We did it in record time. We got the SEBI approval in January 2024 and closed INR 84 Cr of our target within three and a half months. We are now ready to deploy the capital,” said Gulati in an interaction with Inc42 as part of our ongoing Moneyball series.

lockquote>

According to him, the entry of new limited partners (LPs), including a major family office and other veteran investors, is critical to this success. Having a seasoned partner like the ITI Group is another key criterion. The VC firm also leverages the presence of a competent board of advisors, including large asset managers and market players, providing strategic insights into business development.

“Most of our LPs are mature investors seeking diversification. With ITI’s support, we can help them invest across assets to maximise returns,” he added.

Historically, most LPs partnered with big VC funds for secure and profitable investments. But with the private investment scenario undergoing a tectonic change in a post-pandemic world, where agility and adaptability matter most instead of set pieces, smaller but efficient VC firms are gaining traction rather than the VC leviathans.

Let us take you through ITI GO’s investment playbook, its intriguing potential and the measures taken to deliver attractive returns amid economic volatility.

Fund I Investment Thesis And How It Performed In Tough Times

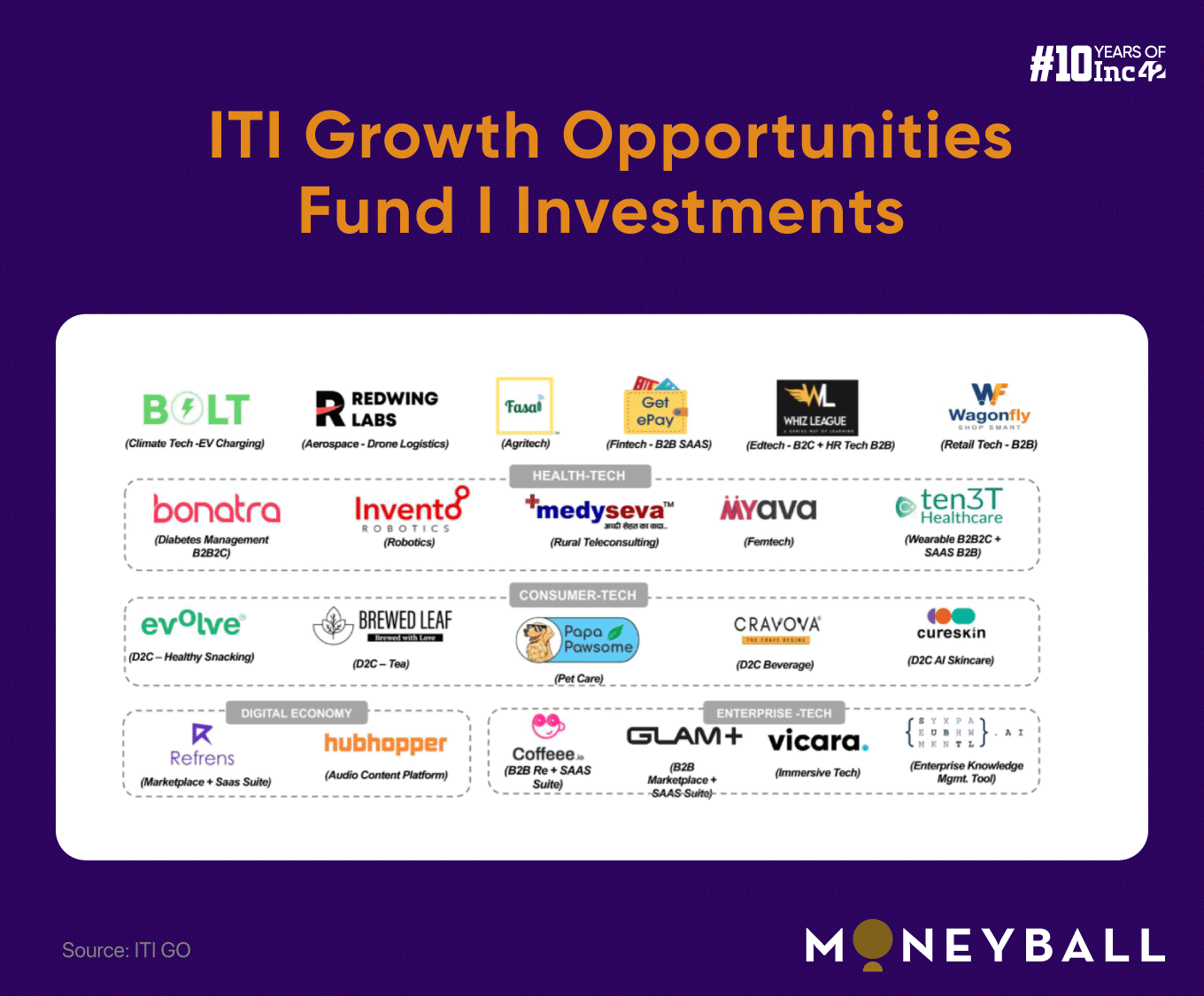

Gulati is sticking to a consistent investment thesis for both funds, believing that successful venture capital investment often requires swimming against the tide and backing resilient founders who can survive against all odds. This has led to early investments in startups such as the all-in-one mobility app Bolt, logistics drone specialist Redwing Aerospace Labs and D2C skincare brand Cureskin, among others.

The VC emphasises that their investments have always been in areas they like and understand. During the funding frenzy of 2021 and 2022, ITI GO made only two investments from Fund I due to skyrocketing valuations and subsequent market corrections.

“However, we made six investments in 2023 when the markets stabilised and we are launching the second fund now,” he said.

lockquote>

The first fund was well-aligned with Gulati’s vision, weathering the test of time and delivering significant returns. ITI GO made 22 investments and exited agritech startup Fasal within a year apart from partially exiting another startup. The fund has an IRR (internal rate of return) of 33% and a DPI (distributed-to-paid-in capital) ratio of 0.45, while four portfolio companies have seen more than 3x valuation markups.

Overall, the fund has achieved a 4.9x valuation markup on deployed capital within 60 months of inception.

lockquote>

While the fund’s core focus areas were consumer internet, healthtech, edtech and the new-age economy, it also invested in aerospace, agritech, fintech, electric vehicles and enterprise tech.

Fund II From ITI GO To Remain Sector-Agnostic

As with Fund I, Gulati prefers not to commit to any specific sector to ensure broader access. While freezing investment and deployment principles for Fund II, the VC has adopted two more strategies.

“About 35% of our fund will be allocated for pre-seed and seed stage investments, while 65% will be reserved for Series A, selective Series B funding and pre-IPO opportunities. In fact, we will have a preferential allotment for some of our portfolio companies heading for IPO. These will ensure a broad deployment spectrum and necessary liquidity to recycle capital,” he said.

Redeploying capital mid-fund will allow ITI GO to opt for fund distribution, returning the money to investors early on. “We are one of the few VCs in India that has managed to return at least half the capital in less than five years while running the first fund. We want to set up a practice where we can return principal investment capital within 5-5.5 years,” added Gulati.

ITI GO Is Not Bullish About Three Popular Sectors

The deal pipeline for Fund II currently features four startups in agritech, wealthtech, consumer internet and edu-fintech. But this time, Gulati is wary of the direct-to-consumer (D2C) space.

“We will approach this sector cautiously while allocating capital from Fund II. D2C is still trying to find its path to scale, and it has been difficult for most brands to progress beyond the initial stage,” he said.

lockquote>

With the emergence of GenAI and the rapid integration of ChatGPT-like technologies across the knowledge industry, Gulati feels that the edtech sector may witness a dip in investor interest. He also has reservations regarding deeptech, believing execution will be difficult in India.

Deeptech startups built on top of intellectual property (in the form of patents, data, know-how, or expertise) may still have potential. However, non-IP products/services (tech commoditised for scale and simplicity) are price takers, not protectable and often lack business control. Spacetech is an exciting area, but Gulati believes the valuations need to adjust for more venture capital investments.

“Nevertheless, we foresee India as a $10-12 Tn economy by 2030, which makes wealthtech a key focus area. India’s wealth is expected to compound at 14-16% annually in the next five to six years, creating numerous opportunities for capital allocation. So, alternative investments are particularly attractive for us,” Gulati pointed out.

lockquote>

AI & Other Tech Tools Assessing Deals, Managing VC Operations

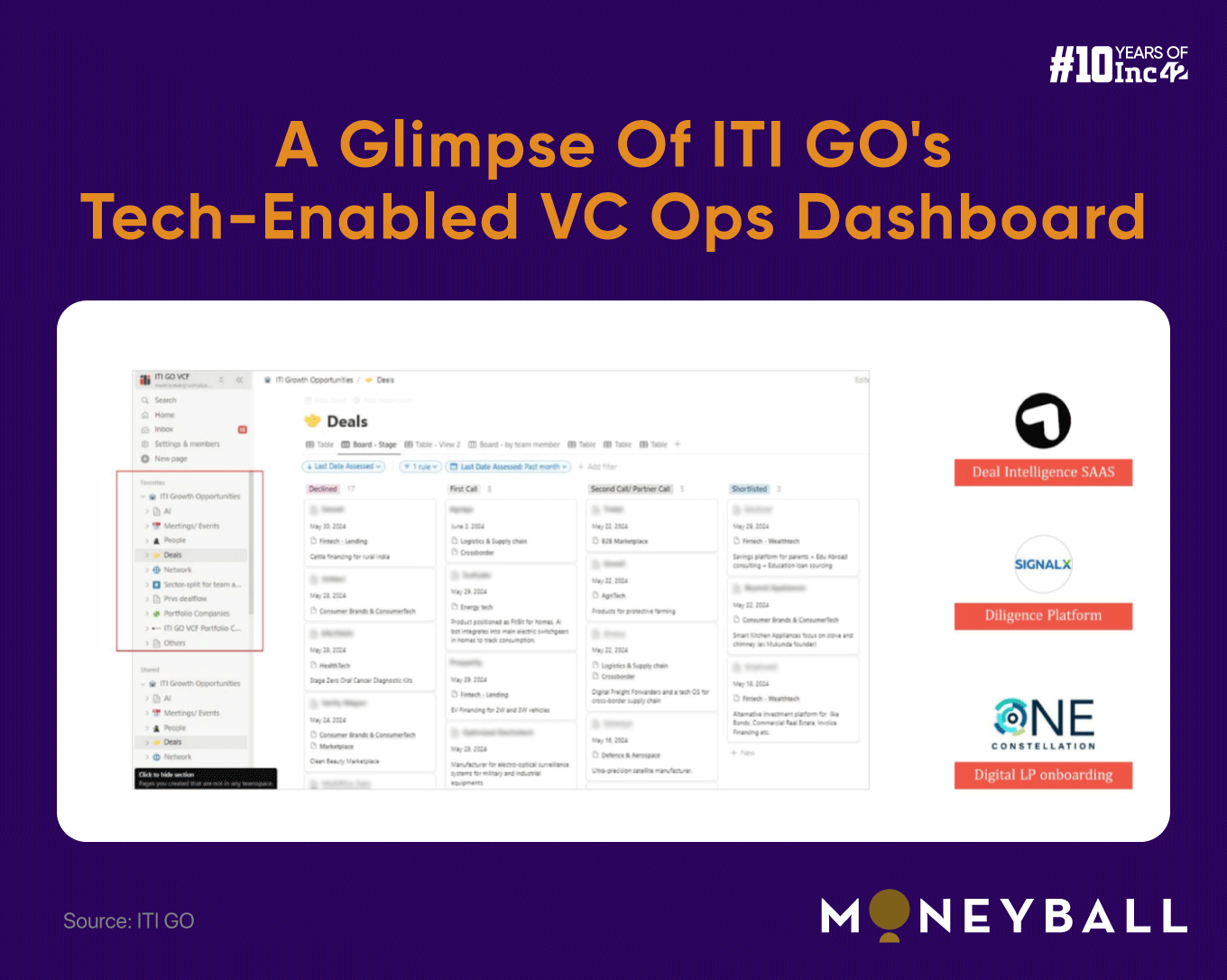

As Gulati and his team soon discovered, running a SEBI-registered fund would offer many learning opportunities. They went through all the nitty-gritty when raising Fund I and strengthened the firm’s internal processes through tech enhancements. These processes help identify focus areas, evaluate strategic investments and time exists effectively as market cycles change.

“We have a comprehensive tracking system for our deal flow and integrated several advanced AI solutions into our evaluation process. It enables us to reach out to entrepreneurs much faster than most VCs in the industry,” he added.

The ITI GO team has also developed an internal ERP for day-to-day VC operations, including deal sourcing, portfolio monitoring, value addition and network expansion. This team will continue to explore and implement advanced technology tools based on AI, data analytics and SaaS to maintain a competitive edge.

Small And Targeted Funds Work Better In India

Globally, the venture capital market is not exactly booming due to an exit drought even after billions of dollars were put into startups in recent years. But for Indian VCs, it can be fairly comfortable going ahead.

Gulati says that venture capital firms in India are uniquely positioned at this point. These are well-capitalised (the country’s PE/VC firms are reportedly holding dry powder worth $20 Bn) and looking for the right investment opportunity.

This capital advantage, coupled with the absence of overseas giants like Tiger Global, SoftBank, Accel and others from the Indian market, presents a promising opportunity for Indian VCs. After a FOMO-driven funding frenzy during the pandemic, major global funds became cautious and rarely took part in mega deals here, given the volatility across the Indian startup ecosystem.

“The next two to three years will be pivotal for Indian venture capital practices. The surge in domestic SIP inflow to INR 18-19K Cr per month makes the capital markets less dependent on foreign investments, although the latter was significantly higher in the past. I see a similar transition in the Indian venture capital market,” said Gulati.

lockquote>

Incidentally, the total amount collected through SIP during May 2024 stood at INR 20,904 Cr per an AMFI report, compared to INR 14,749 Cr in the year-ago period, a 41.73% jump. If this indicates improved risk appetite at the retail level, it is hardly surprising that 270+ Indian investors, with a cumulative corpus of $33.72 Bn announced during 2021-2023, will only be too eager to track bright business plans and hit landmark moments.

The ITI GO founder also anticipates further development of patient capital, as investors are willing to adopt a long-term approach and build businesses from the ground up. LPs are also more proactive, driving the investment momentum. Raising INR 84 Cr for Fund II within three months and a half with zero distribution speaks amply of active commitments from LPs, says Gulati.

Moreover, a non-distributed fund (where fund managers need not split their fees with external entities), even if it is a small one, ensures a higher margin and enables quicker capital returns due to better performance. In contrast, it is challenging for an INR 2K Cr fund to be fully invested and returned, given the limited depth of the Indian market. Only one or two funds in India can do this.

“Therefore, our strategy is to focus on raising smaller, targeted funds. We plan to raise INR 300 Cr for Fund II and will continue to raise similar amounts for the next funds. This will ensure healthy cash flows across all funds, which is difficult to achieve when pursuing an ultra-large fund,” concluded Gulati.

lockquote>

[Edited by Sanghamitra Mandal]

Disclaimer

We strive to uphold the highest ethical standards in all of our reporting and coverage. We StartupNews.fyi want to be transparent with our readers about any potential conflicts of interest that may arise in our work. It’s possible that some of the investors we feature may have connections to other businesses, including competitors or companies we write about. However, we want to assure our readers that this will not have any impact on the integrity or impartiality of our reporting. We are committed to delivering accurate, unbiased news and information to our audience, and we will continue to uphold our ethics and principles in all of our work. Thank you for your trust and support.