SUMMARY

All fintech intermediaries or business payment service providers offering credit cards to corporates for business transactions will be impacted by the RBI’s decision

While Mastercard has also been speculated to be facing the RBI’s scrutiny, there remains a lack of clarity regarding the impact on other card networks

The RBI’s regulatory actions on fintech startups have been relentless since June 26, 2023, when it directed PPI issuers to cease UPI in cobranding arrangements

On February 15, 2024, the Reserve Bank of India (RBI) directed an unnamed card network to halt all card-based business payments made via payment intermediaries to entities that do not accept card payments with immediate effect.

As per industry sources, this was a special arrangement brought in by the card network Visa. Other card networks operational in India include Mastercard, RuPay, American Express and Diner’s Club.

While Mastercard, too, has been speculated to be facing RBI’s whip, there has been no clarity on the impact on other card networks.

Banks have also been asked to halt all payments made via commercial credit cards through the card network in question. Fintech intermediaries facilitating these transactions have also been asked to stop all transactions with immediate effect.

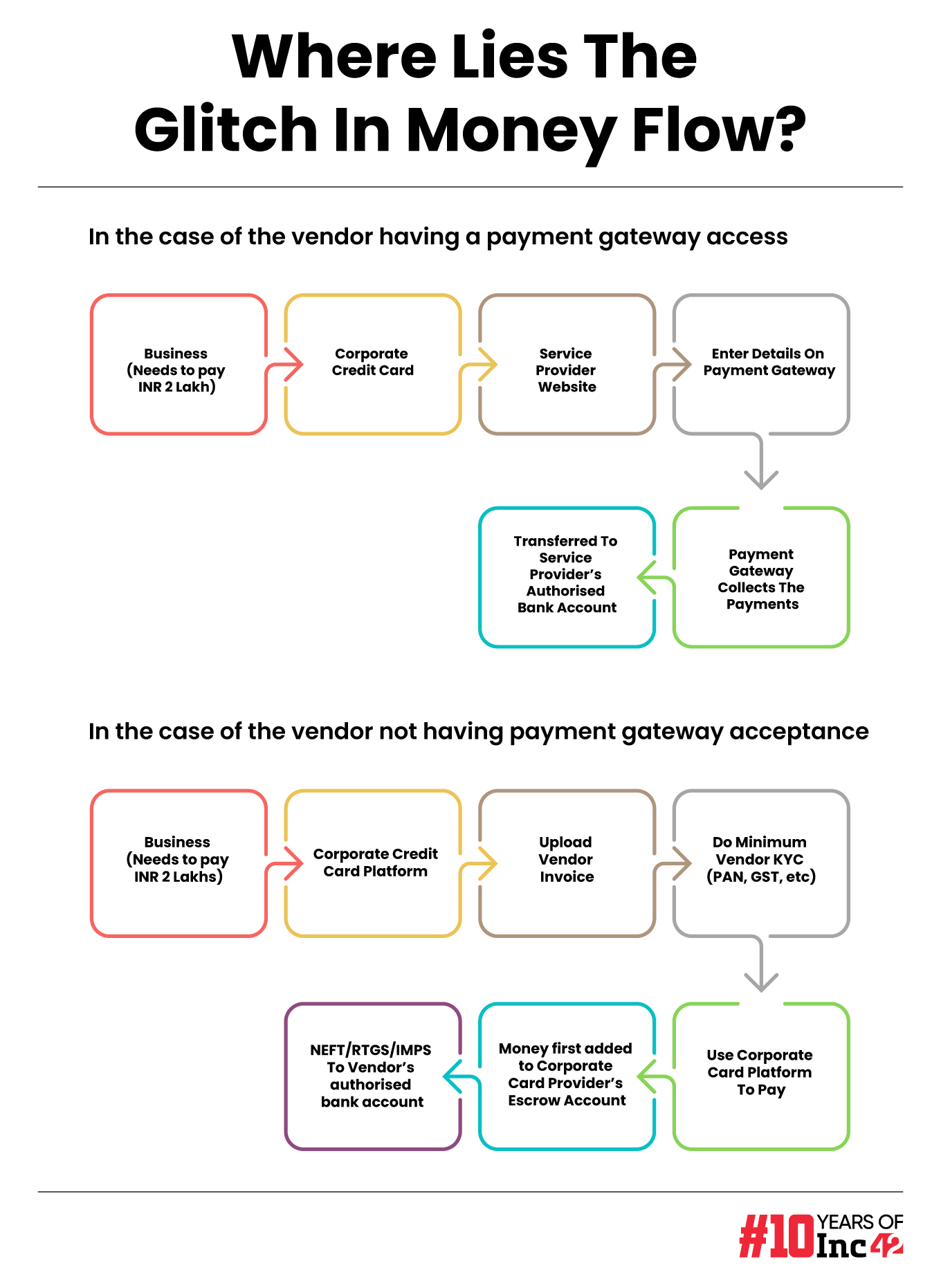

“This is not a ban on corporate credit cards, but a specific use case being highlighted by the RBI. This is a freeze on using your corporate credit card to make payments to vendors who do not have a payment gateway acceptance,” sources close to the development told Inc42.

lockquote>

Who Will Be Impacted?

It is imperative to note that not all fintech intermediaries or business payment service providers (BPSP) offering credit cards to corporates for business transactions will be impacted.

BPSP is not a regulated space. It is more an industry term used for fintechs offering these services to businesses.

As explained by an industry expert — when a business or a business employee has a corporate credit card, they can use it for travel bookings, or to pay for SaaS subscriptions. These transactions are considered valid as these organisations have been onboarded as merchant partners by payment aggregators such as RazorPay.

However, in the case of small vendors — for example, a company taking care of an office’s blue-collar workforce, who only accept payments through bank transfers or cheques, the business will have to either use cash in the account to pay or take a loan in some form to make the payment against the invoice in case of cash crunch.

“Instead, the fintechs acting as business payment service providers (BPSP) would allow the business to use their limit on the credit card to make payment to that vendor. Businesses get an interest-free credit line for 45 to 60 days for which they pay an MDR fee – so a cheaper access to credit vs other sources. To the vendor, it will be like any other credit into their bank account. Which is why it was a popular use case, although not according to the letter of the law,” a source said.

lockquote>

As of now, there is no clarity on how many of the BPSP fintechs will be impacted.

“While most fintechs started corporate credit cards as a means for businesses to manage their employee expenses, most players have added vendor expense management and settlement as an additional feature. Considering this, a majority of the BPSP players will be impacted in some or the other way,” another industry source said.

What’s Illegitimate As Per RBI?

Under the PSS Act 2007, Section 2(1) (i), a payment system means:

- A system that enables payment to be effected between a payer and a beneficiary, involving clearing, payment or settlement service or all of them.

- A “payment system” includes systems enabling credit card operations, debit card operations, smart card operations, money transfer operations or similar operations.

Further, in terms of Section 4 of the PSS Act, 2007, no person other than the Reserve Bank can operate or commence a payment system unless authorised by it.

In the present case, the card network has not taken the RBI’s approval to act as a payment system. As of now, only those with licences such as prepaid payment instruments, payment gateways and payment aggregators can be considered valid payment systems.

According to the RBI, the card network had an arrangement that enabled businesses to make card payments through certain intermediaries to entities that do not accept card payments. The activity was, therefore, without legal sanction.

This is a shocking move for the ecosystem. As Aditi Oleman, senior director-product marketing and strategy at Cashree mentioned in a LinkedIn post, “the ecosystem is yet to figure out what led to the freeze by RBI on this business, which has sponsorship of banks and all the large card networks.”

However, there are various ways that such transactions could run afoul of RBI’s regulations.

For instance, companies could hide the trail of money flow by using intermediaries, and the eventual destination of funds paid to intermediaries is not clear.

According to industry experts, the inability to see the transaction trail from BPSP’s escrow account to the vendor’s bank account could lead to money laundering or round-tripping of funds.

“I could be sending money to my friend’s account or a newly set up vendor and can then re-route it back to me as cash or to my wallet. It will not be easy to track and there is no end-to-end visibility,” a source said.

lockquote>

Companies could also use corporate credit cards for personal use, like paying rent, when such cards should ideally be only used for business purposes or to upload fake invoices against which they make the payments.

What Is The Way Out?

The RBI’s regulatory actions on fintech startups have been relentless since June 26, 2023, when it directed prepaid payment instrument (PPI) issuers to cease UPI in cobranding arrangements.

From e-mandates to tokenisation and from digital lending to payments banks, the RBI is plugging all loopholes in the country’s fintech space. Unfortunately, this is leading to the death of many fintech companies in the process.

Decentro’s CEO Rohit Taneja sees virtual accounts as a solution for compliant and seamless transactions through payment aggregators.

lockquote>

Many businesses have also started asking their vendors to refresh KYC details to get onboarded again to the payment gateway or payment aggregator.

The ecosystem hopes that instead of completely shutting it down, the RBI will come up with guidelines on how to make BPSP’s operations transparent.

Everything said and done, the question remains: Will adhering to RBI regulations stifle fintech innovation? Abrupt decisions can harm investor sentiments and the fintech industry’s entrepreneurial spirit.

Regulations are a reality for startups, but some founders argue for a balance, suggesting regulators leave room for innovative products and services.

[Edited by Nikhil Subramaniam]

Disclaimer

We strive to uphold the highest ethical standards in all of our reporting and coverage. We StartupNews.fyi want to be transparent with our readers about any potential conflicts of interest that may arise in our work. It’s possible that some of the investors we feature may have connections to other businesses, including competitors or companies we write about. However, we want to assure our readers that this will not have any impact on the integrity or impartiality of our reporting. We are committed to delivering accurate, unbiased news and information to our audience, and we will continue to uphold our ethics and principles in all of our work. Thank you for your trust and support.