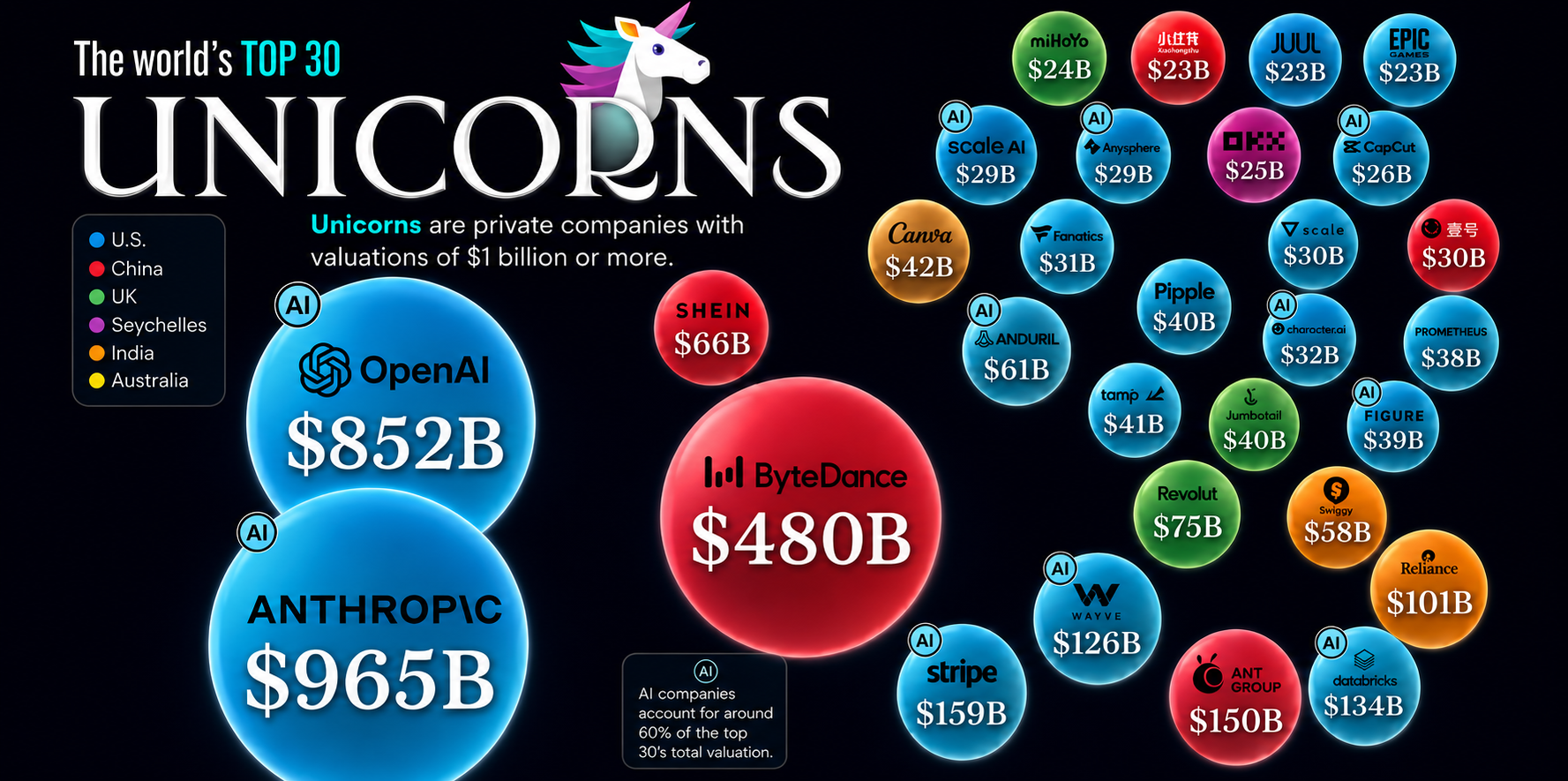

AI companies like Anthropic & OpenAI now lead the world's highest-valued private startups, making up nearly half of the $3.9T total.

The global private markets are witnessing a profound reordering, with artificial intelligence companies now commanding the pinnacle of unicorn valuations, fundamentally altering investor risk appetites and strategic allocations. New data for 2026 reveals that AI giants Anthropic and OpenAI alone account for nearly half of the combined $3.9 trillion valuation across the world’s 30 most valuable private firms, signaling a concentrated shift of capital and technological focus.

This unprecedented concentration in AI reflects a seismic shift from the previous era dominated by fintech, e-commerce, and social media platforms, indicating a maturation of venture capital's focus toward foundational technological advancement. The United States maintains its preeminence in fostering these mega-unicorns, underscoring the depth of its capital markets and a robust ecosystem for scaling disruptive innovations. The data, sourced from Crunchbase, quantifies these valuations based on each firm’s latest reported private funding rounds.

Anthropic leads the ranking with an astounding $965 billion valuation, closely followed by OpenAI at $852 billion. These figures not only highlight the immense investor confidence in generative AI’s transformative potential but also present a unique challenge for traditional valuation methodologies, often struggling to contextualize such rapid and speculative growth. The sheer scale of these companies is redefining what constitutes a "unicorn," pushing the boundaries of private market capital formation.

What It Means

The ascendancy of AI companies to the apex of private market valuations carries significant implications for the broader technology sector and global investment landscape. This trend suggests a deepening conviction among investors that artificial intelligence represents not merely an incremental technological advance but a fundamental paradigm shift akin to the internet's advent, capable of reshaping every industry from healthcare to finance.

The dominance of AI firms, accounting for roughly 60% of the top 30 unicorns' combined valuation, indicates a strong flow of capital into a relatively narrow segment of the tech market. This concentration could lead to further consolidation in the AI space, with larger, well-funded players potentially acquiring smaller innovators, thereby exacerbating market power dynamics. For venture capitalists, it means an intensified focus on identifying and backing the next generation of AI breakthroughs, often necessitating larger, later-stage funding rounds that challenge traditional fund structures and risk profiles.

This shift also implies a reevaluation of what constitutes defensible moats in the tech industry. While network effects and platform scale previously drove valuations for social media and e-commerce giants, AI companies are increasingly valued for their proprietary data sets, advanced model architectures, and the computational infrastructure required to train and deploy sophisticated algorithms. The race for AI talent and computing resources is becoming a critical determinant of success, driving up operational costs and further favoring those with substantial capital backing.

Anthropic and OpenAI, the two leading AI giants, command a combined private market valuation exceeding $1.8 trillion, representing nearly half of the total value for the world's 30 most valuable unicorns.

The Context

The current landscape of unicorn valuations is a product of several converging trends that have reshaped global venture capital over the past decade. The proliferation of accessible cloud computing, advancements in machine learning algorithms, and a global talent pool increasingly proficient in data science have collectively fueled the AI boom. This build-up phase has culminated in the breakthrough capabilities of generative AI, which captured public and investor imagination in the mid-2020s, accelerating investment velocity.

Historically, private market valuations have ebbed and flowed with broader economic cycles and investor sentiment. The period leading up to 2026 saw an unprecedented availability of growth capital, driven by low interest rates and a hunger for high-growth assets, which allowed companies to remain private for longer and achieve stratospheric valuations before contemplating public offerings. This environment fostered the rise of "mega-rounds," where companies raised hundreds of millions, or even billions, of dollars in single tranches, pushing valuations well into the tens and hundreds of billions.

While U.S. companies continue to lead global unicorn creation, reflecting the maturity and depth of its venture capital markets and access to cutting-edge technical talent, the list of top-valued private firms highlights a geographically diverse innovation landscape. China, India, the United Kingdom, Australia, and even smaller financial hubs like Seychelles are represented, showcasing a global distribution of entrepreneurial activity. ByteDance from China, with its $480 billion valuation, remains a formidable player, demonstrating the scale achievable in non-AI sectors, particularly in consumer internet and entertainment.

Beyond the immediate AI fervor, other sectors continue to house significant private value. Fintech remains a robust category with companies like Stripe ($159 billion), Revolut ($75 billion), Checkout.com ($40 billion), and Ramp ($44 billion) reflecting sustained demand for digital financial services and infrastructure. Similarly, e-commerce platforms like Shein ($66 billion) and mobility solutions such as Waymo ($126 billion) continue to attract substantial investment, albeit overshadowed by the explosive growth in AI.

The Bear Case

Despite the overwhelming enthusiasm surrounding AI unicorns, a contrarian perspective suggests several latent risks that could temper their unprecedented valuations. The sheer scale of capital deployed into these few entities raises questions about market efficiency and potential overvaluation, echoing sentiments from past tech bubbles. The high burn rates associated with AI development, particularly for large language models requiring immense computational power and specialized talent, demand continuous, significant capital injections, making these companies highly sensitive to shifts in investor sentiment or capital availability.

Regulatory scrutiny also looms as a significant headwind. Governments worldwide are grappling with the ethical, societal, and economic implications of advanced AI, potentially leading to stringent regulations on data usage, algorithmic transparency, and market concentration. Such interventions could impose substantial compliance costs, restrict operational models, or even break up dominant players, directly impacting future growth trajectories and profitability. Furthermore, the rapid pace of AI innovation itself presents a challenge; today's leading models could be superseded by unforeseen architectural breakthroughs, making current technological moats potentially ephemeral.

The path to profitability for many of these hyper-valued AI companies remains opaque. While their underlying technology is transformative, converting immense research and development into sustainable, scalable, and diversified revenue streams at a pace that justifies current valuations is a formidable task. The highly competitive landscape, with both established tech giants and a continuous stream of new startups entering the fray, further compresses potential margins and makes long-term market dominance far from assured.

Investors will be closely monitoring several key indicators over the coming quarters, including the tangible progression of these AI unicorns toward diversified revenue generation and sustained profitability. Upcoming major funding rounds will provide insights into continued investor appetite and valuation benchmarks. Additionally, any significant regulatory pronouncements from global bodies regarding AI governance or antitrust measures will be crucial catalysts. The eventual initial public offerings of these giants, whenever they occur, will serve as a critical test of private market valuations against public market scrutiny, potentially reshaping the broader tech index.

Frequently asked questions

What are the most valuable unicorns in 2026?

In 2026, the world's most valuable unicorns are led by AI companies Anthropic and OpenAI. Anthropic is valued at $965 billion, while OpenAI stands at $852 billion, together accounting for nearly half of the top 30 unicorns' combined valuation.

Which industry dominates unicorn valuations in 2026?

Artificial intelligence (AI) companies overwhelmingly dominate unicorn valuations in 2026, accounting for roughly 60% of the combined $3.9 trillion valuation of the top 30 firms.

How much are Anthropic and OpenAI valued at in 2026?

Anthropic is valued at $965 billion, and OpenAI at $852 billion in 2026, making them the two most valuable private companies globally.

What is a unicorn company?

A unicorn company is defined as a private firm with a valuation of $1 billion or more. These companies represent the highest-valued private startups in the global market.

Where does the data for unicorn valuations come from?

The data for these unicorn valuations is sourced from Crunchbase, reflecting each firm’s latest reported private-market valuation as of 2026.

Are there non-AI companies among the top unicorns?

Yes, while AI dominates, other industries like fintech (Stripe, Revolut), e-commerce (ByteDance, Shein), and mobility (Waymo) also feature prominently among the world's most valuable unicorn companies.